LM2 - C4 - Market Security

LO C4

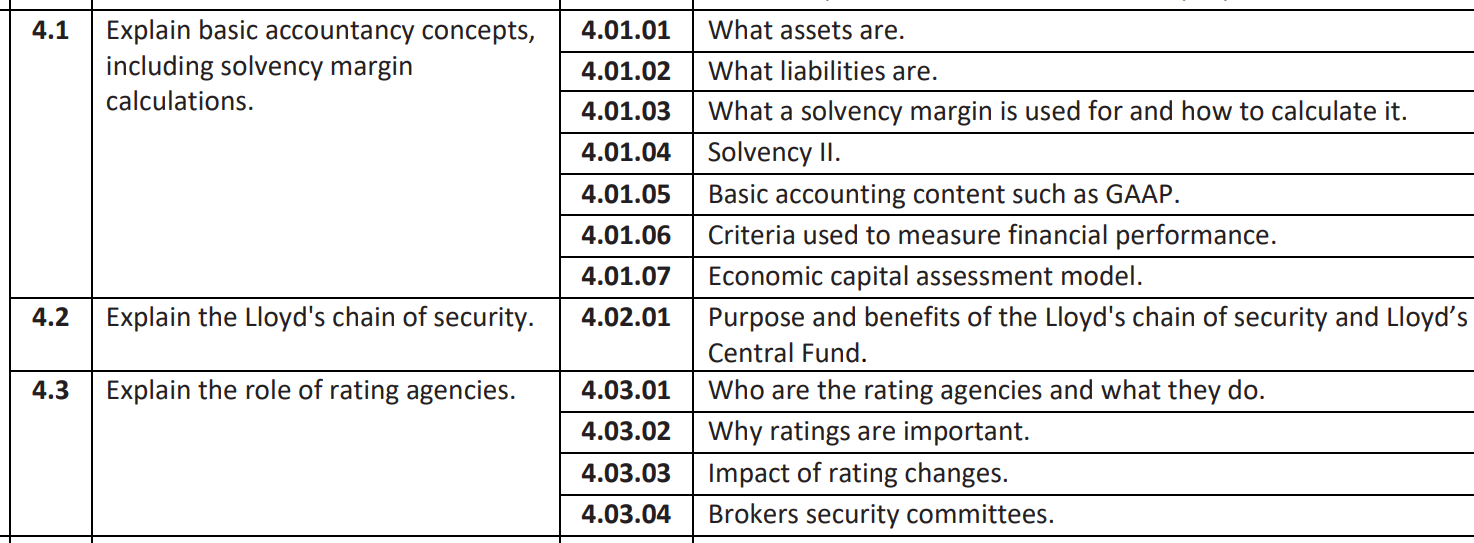

4A) Solvency

Assets >= paid claims + unpaid claims + Ops cost

Solvency means more assets than liabilities:

Of which Unpaid claims falls into 2 categories:

IBNR vs IB

"incurred but not reported"

- IBNER for reported claims that will develop above current case reserves

- IBNR for claims that have happened but are not yet reported often associated claims handling expense reserves as well

Margin is amount assets exceeds liability, improve ability to pay future claims. Why?

- COB have different volatility, long vs short tail LM2 - C2 - Risk Written in London Market

Incurred But Not Reported (IBNR) - Claims that are not yet known about but need to be factored into overall reserving calculation

IBNR does not directly become IBNER; once reported, it becomes a known claim, and any later underestimation on that known claim is IBNER.

Basic Accounting

- Assets - Items of value, resources a business owns or controls (building vs goodwill).

- Premium + Investment returns ARE Assets

- Capital - Working capital difference between assets and liabilities

- Liabilities - Monies owed to others.

- Claims paid or outstanding.

- Cost of reinsurance + biz ops

- liquidity (Can be solvent high assets BUT illiquid),

Ratio

loss (claims/premium),

combined ratio (Ops cost + claims / premium and investment income)

Combined ratio = (Claims incurred + underwriting or operating expenses) / earned premium

Float = Unearned premium, Outstanding claims reserves, IBNR

pool of money an insurer holds between receiving premium and ultimately paying claims.

Liabilities = increasing premium and claims by 50%

Reinsurance cost

4B) Solvency II

Introduced via PRU

pan-EU regime

Solvency II rules apply to all insurers, reinsurers, captives, mutuals, with their head office in the EU, Lloyd’s Europe

Objective: pay policyholders claims when needed.

- Better regulation

- integration of EU insurance market

Pillars for Solvency II:

- Quantitative requirements - Based on Business risk INSURERS determine

- **Solvency Capital requirement (SCR) = how much above liabilities.

- lower amount = minimum capital requirement (MCR) REGULATORS INTERVEN

- Supervisory review - Own risk & solvency assessment (ORSA)... internal review undertaken by insurers

- Disclosure - publicly disclosure more information

Risks faced by INSURERS

- Counterparty risk (premiums not paid, reinsurance claims)

- Operational risk ( outside authority UW, access systems/buildings)

- Market risk (Investments failing, Exchange rate losses)

- Liquidity risk (Release investments quickly, cash flow issues)

- Group and capital risk (writing lines on same risk, reinsurance coverage, claims pilling, )

- ERM ()

Financial Services and Markets Act 2023 - UK reg own regulation approved by EU

Why regulators needed in Solvency II

European Insurance and Occupational Pensions Authority (EIOPA)

- protection for consumers

- effective and consistent...

Brexit → temporary carry-over rules → FSMA 2023 brings rulemaking back to UK regulators → equivalence is separate and area-specific.

4C) Lloyds chain of security

Central Fund is a pot of money

- Syndicate level assets = Written premium to pay claims

- Members fund = Syndicate members deposit funds in Lloyds. Amount determined by SCR + ECA

- Central assets = Last resort all members contribute 0.35% of premium

4D) Rating agencies

Middle man which publishes their results for public consumption.

- S&P

- Fitch

- A M Best

- Moody's

Claims, operating performance (which includes factors such as the quality of the management of the business, and past profitability); and business profile.

Using rating

Brokers and insurers have security committees.

- What is the rating for insurers brokers care to place clients business.

- terms and conditions offered

- broker could be exposed to a claim for professional negligence from their client.

If an insurer’s rating falls, it might find that it’s considered unacceptable as a market and will lose business

Broker liable for claims if the rest of the market was NOT downgraded at the same time as the insurer’s individual downgrade.

C4 Key Points