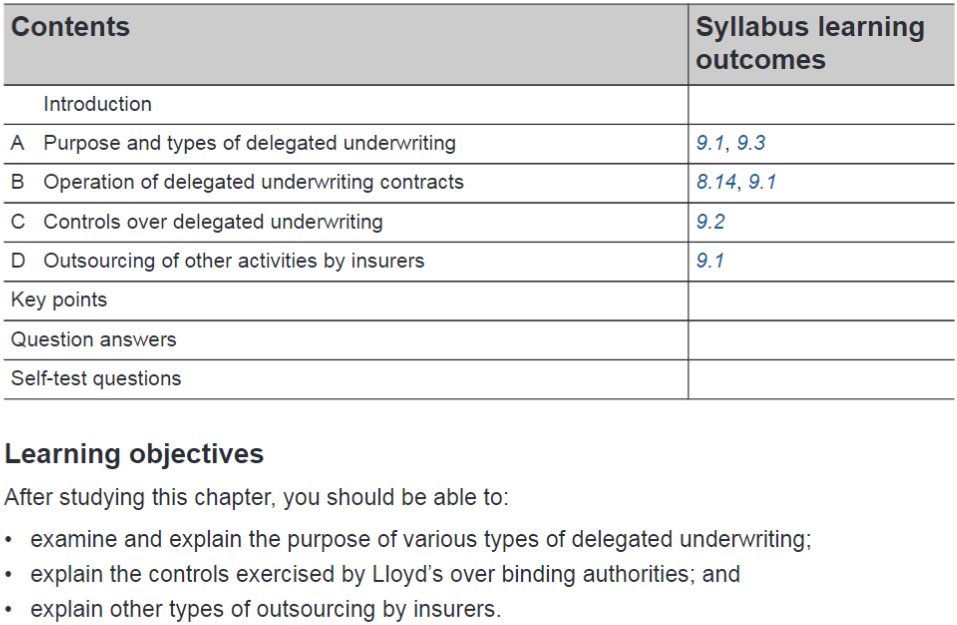

LM2 - C9 - Delegated Underwriting

LO C9

binding authorities = cover holder or service company

or Someone who holds authority granted under a binding authority

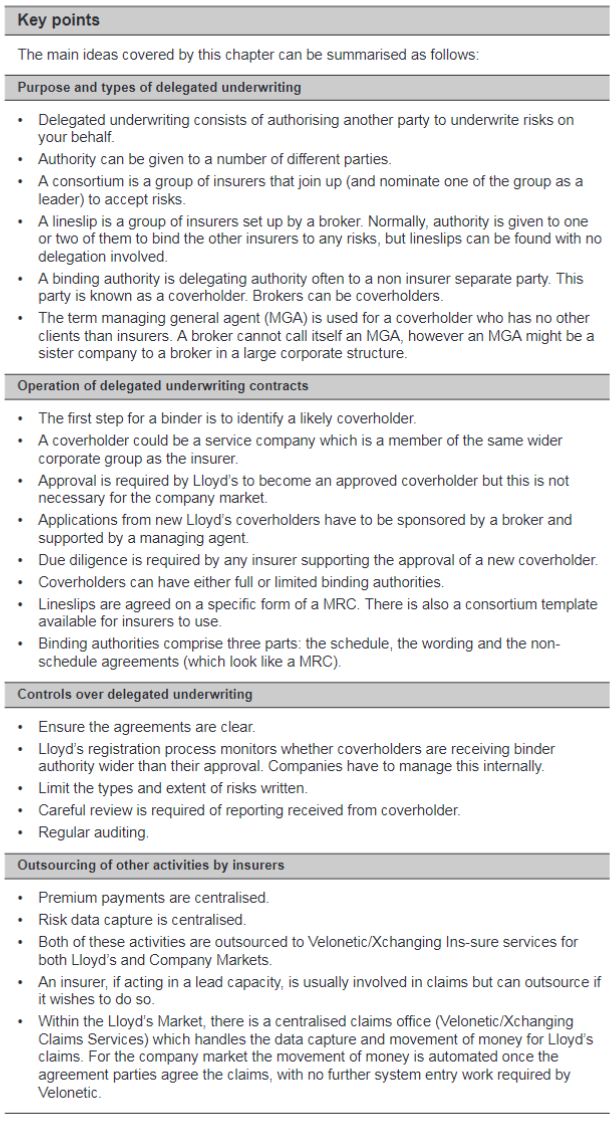

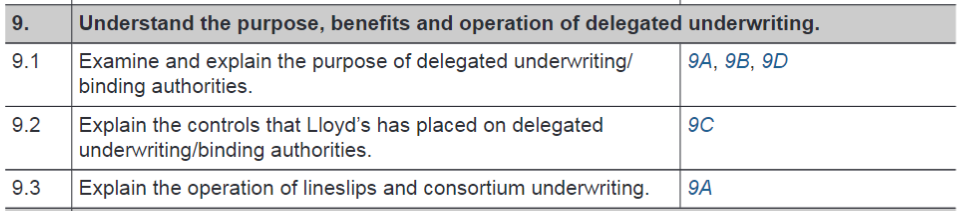

9A) Purpose and types of delegated underwriting

An insurer can choose to delegate underwriting authority to:

- Another insurer (or set of insurers)

- A broker or

- Another entity altogether.

Setting up a new Coverholder: Company market vs Lloyd’s market

Company market insurer

- Can appoint a coverholder using its own internal approval processes

- No external approval is required

Lloyd’s syndicate - Must obtain Lloyd’s approval before delegating underwriting authority

- This reflects Lloyd’s role in managing, supervising, and protecting the Market

Sponsorship by a any managing agent. Coverholders represents lloyds, the insurer and has policyholder protection.

Managing agent must do DUE DILIGENCE... can their underwriting be trusted. Are individuals experienced? systems and controls? financial standing? REGULATORY AUTHORITY

MUST submit an ATLAS to lloyds, information centrally stored

Types of Coverholders

2 Main type

- "Approved Coverholder" - CFC underwriting

- Service company Coverholder - setup by managing agent (Binding authority from the syndicate, extension eg Ark opens office in Singapore)

Allows access to more business overseas also can do motor insurance

Types of authority for Coverholders

- Full authority - complete underwriting control

- pre-determined rates - Insurer provides a rating matrix. match market pricing

- pre-determined rates no discretion - No changes to rating matrix

- prior submit - approved before it can be bound.

Limits placed on risk details,

Operation of joint certificate

Bind authority legal and operational agreement that gives a coverholder delegated authority to bind risks on behalf of a syndicate.

schedule

- all the details of the delegated authority:

non-schedule agreements

Binding authority registration date and number - time bound regulated by Lloyds.

9.3 Function of Consortium (Ark 9585) and Lineslip (MORE facility)

If Delegation to another insurer (or set of insurers)

Consortium:

Leader accepts or declines risks on behalf of the consortium, set up for a year.

- Ark Renewable does this because... profitable, efficient, commission.

- Smaller risks broker like processing consortiums

LM2TB6_2026_online, page 236

Lineslip (Facility another term) pre-arranged agreement:

Insurers brought together by a broker

- MRC lineslip with terms + conditions. 1-2 insurance leader agreeing RISK ATTACHING

- Brokers like a pre-agreed group of UW.

- Broker processing advantages & follow market attachment

- Have commissions or fees for leaders within lineslips – meaning fewer advantages for a lineslip leader

Therefore Lineslip = Framework

via a Declaration = Individual contract

If individual risk is presented by broker attaching to the Lineslip.

Declaration (different contract). A declaration is the mechanism by which risks attach under that facility.

via a Bulking OR non-bulking Lineslip: One-by-one declaration

Terms indicate whether the broker can aggregate premium presentations into Velonetic (bulking lineslip)

OR

Whether the premium for each risk declared under the Lineslip must be presented individually (non-bulking Lineslip).

- easier for the broker to administer, but more difficult for the insurers to determine easily how much premium relates to which risk.

Lockton BESS facility and Marsh MORE facility examples of lineslips

Delegation to a broker or another entity

‘binding authority’ or ‘binder’ = insurer to delegate underwriting authority either to a broker.

9B) Operations of delegated underwriting contracts

Decision to delegate some underwriting authority

- Resources: Insurer to underwrite everything directly

- Local access: Insurer doesn't want to set up offices out of London

- Other access: Class of business

How to select partner to delegate authority (Coverholder):

- Profession reputation

- Niche product/territories

Conflict of interest may arise & managed

Conflict of interest

- Placing risk

- Handling claims

broker supposed to act in the best interest of their insured clients. However, if they are a coverholder for an insurer then they are acting as their agent and so conflict when selecting insurers in the risk placement process.

CREATE an ETHICS WALL

manage conflict of interest

9C) Controls over delegated underwriting

Controls Lloyds have placed over Delegated Underwriting/binding authorities

Principles 1,4,5,11 for doing business at Lloyd’s

- Underwriting profitability: appetite, process control, business plan, cost incurred, pricing strategy

- Claims management: Delegated claims handling = consistent

- Customer Outcome:

- Regulatory and financial crime:

Contract certainty LM2 - C8 - Business process key details about levels and extent of authority are captured.

Clarity of agreement setting out levels of authority

Registration

registration of all binding authority agreements (except restricted authority agreements).

Delegated Contract Oversight Manager (DCOM) = Lloyd’s to capture information about the contracts being entered into with each coverholder + Ristriction placed on coverholder

Reporting

monthly or quarterly bordereaux reporting. take in data clean and report. eg consotrium partners needs to check what risks have been written.

OR

Coverholder sends data to insurer for them to calculate P&L

Documentation

Insurer should always ensure that the documentation that is being issued by any coverholder complies with the binding authority agreement (e.g. including a several liability agreement),

Auditing

Physical audits on coverholder required. frequency, scope of review, details, underwriting, accounting, IT

9D) Outsourcing of other activities by insurers

Outsourcing and delegation are in fact the same.

- One party is requesting and empowering another to perform tasks on their behalf subject to an agreement as to the extent of the authority given.

- Premium and risk keying functions are performed by an Velonetic company (Xchanging Ins-sure Services).

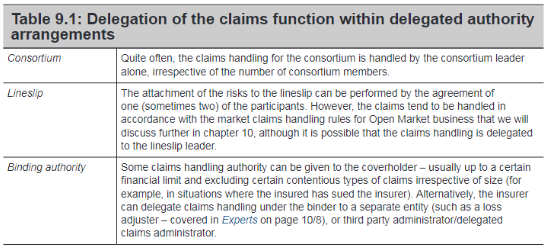

Claims handling within a consortium, Lineslip or binding authority LM2 - C10 - Claims handling

Key points C9