LM2 - C6 - Insurance intermediation in London

LO - Brokers in London

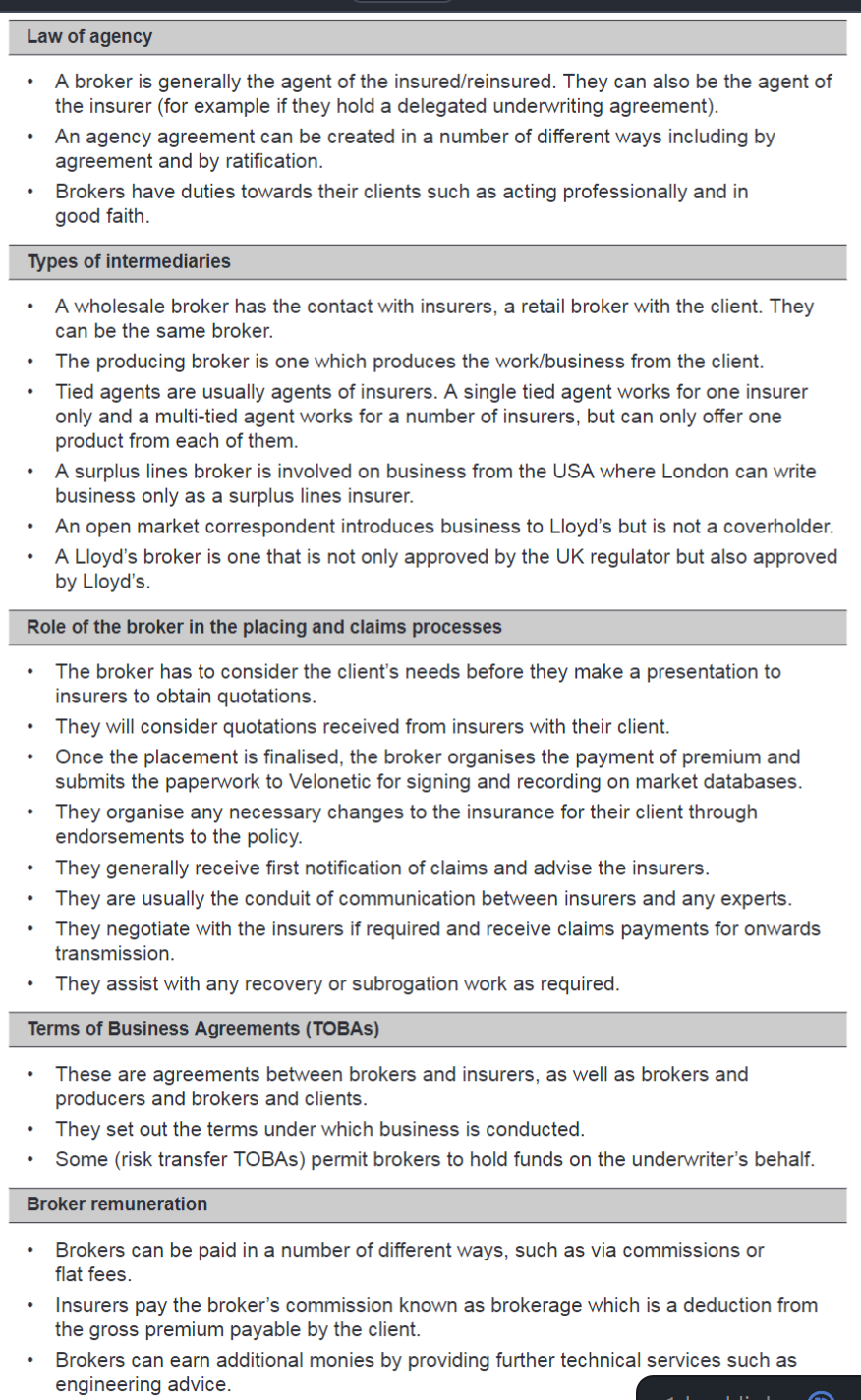

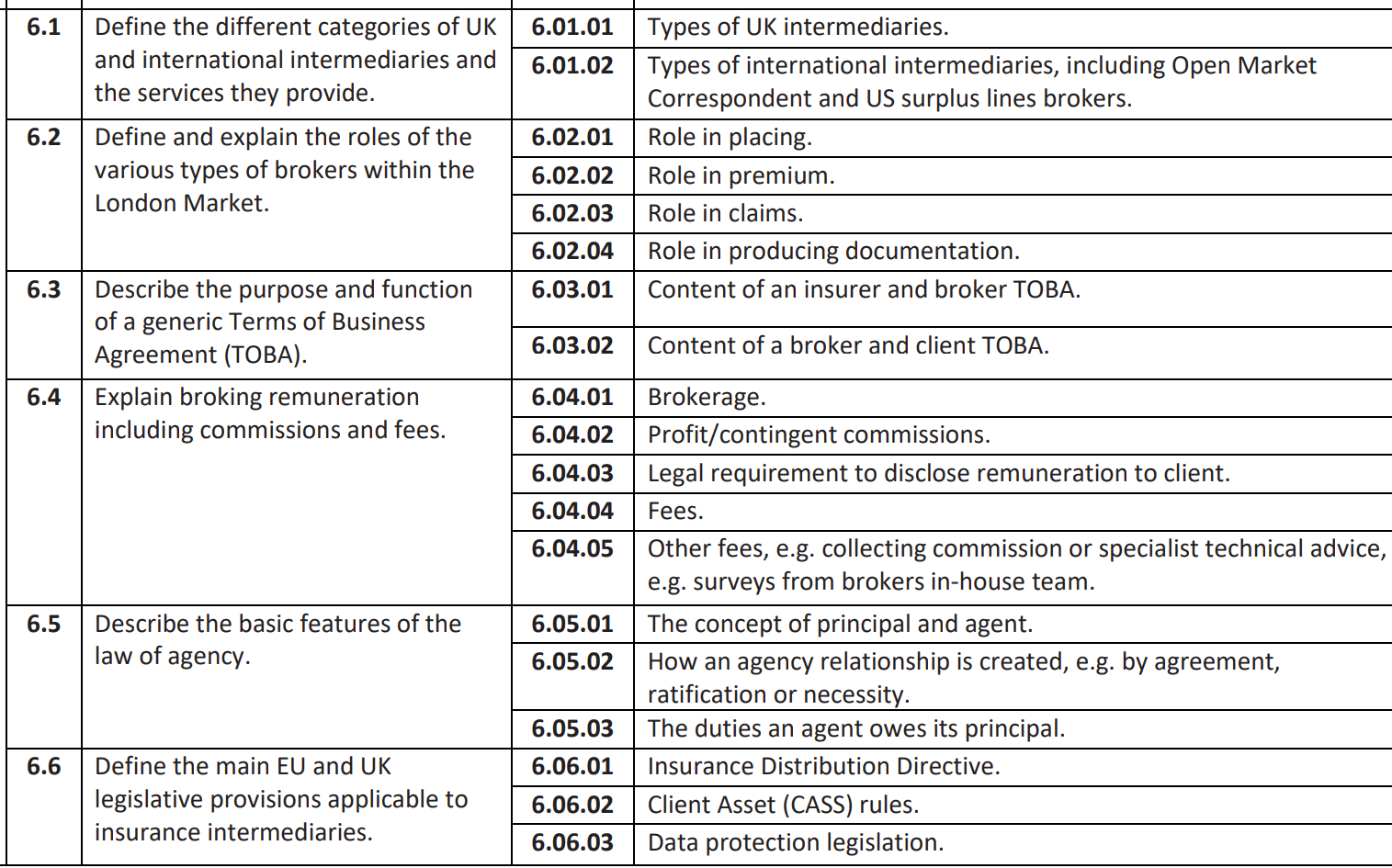

6A) Law of agency = Beware conflict of interest

Insurer gives authority to broker but is also responsible to insured. NEED "ethics wall"

AGENCY AGREEMENTS:

- By agreement - writing

- By Ratification - behaviour accepted/condoned after action taken

- By necessity - last resort, emergency someone has to make a decision, as no-one with actual authority to do so is present

Duties towards principles

- No sub delegate without permission

- Good faith

- Follow instruction

- Accounting and skilled

PRICIPLES CAN

- ratify,

- Ratify and claim for damages

- refuse to ratify their actions and expose the agent to claims from the third party that thought the agent was acting within their authority 3rd party claims

When clauses are introduced think why now?

Principles can file for

Professional negligence against brokers/intermediaries

If

- ensuring that the insurance was placed with suitable insurers;

- ensuring that the insurance was placed on suitable terms and conditions;

- ensuring that they understood the client’s instructions;

- explaining terms (such as warranties) and their effect on the client.

6B) Types of intermediaries

- Wholesale - closest to insurer (People I email)

- Retail - Closes to Client

- Producing broker - supports clients with documents

- Surplus line broker - (local USA not able to take risk on)

Others

- Single tied agent - car insurer feeder

- multi tied agent - multi line insurers

- independent intermediary - FREE AGENT BROKER for client

- Open Market Correspondent (OMC) - Client => Local broker (OMC) => Lloyd’s broker => Lloyd’s syndicates (think Canada and Italy) https://www.gassltd.ca/services/energy/

Broker who PASS REGULATORY can obtain Lloyd’s accreditation.

6C) Role of broker in Placing & Claims

Placing - Think about car insurance PROCESS

-

Reviewing Client's needs… is exclusion leg3 required, Securities committee

-

Putting together a SLIP/MRC to obtain quotes… survey, loss record,

-

What are the difference between quotes?

-

Finalise placement: premium payment clauses (pro rate)

-

SUBMISSION to VELONETIC: Taxes, each stakeholder is liable + Accounting & Settlement

-

Request premium from client

-

Submitting documents to velonetic allow upload to IMR give signing number & date

-

Finally: On risk and make changes via Endt.

EMAIL or PPL What types of information is included in the submission…

Influence judgement of underwriter in considering a risk

Insurers LM2 - C4 - Market Security#4D) Rating agencies

Claims:

- First advice: Presentation made considering the claim.

- Expert Instruction: Independent via insurer or assigned by broker, Fees liable to insurer

- Negotiation with claims: If hairy

- Settlement: insurer pays broker to then pass towards insured.

- Subrogation

LM2 - C10 - Claims handling#Brokers role in claims process

6D) TOBA what's inside

A broker has TOBAs with insurers, clients and possibly also with ‘producing brokers’.

High level

AGREEMENT WITH - managing agent + intermediaries

- Regulatory status

- Authority - HOLD insurers fund (Yes or NO)

- Remuneration - How it will be set on in individual contracts

- Taxes

- Data - REDUCE AMBIGIOUTY how recipt of data shown and protection act 2018 GDPR

- Confidentiality - transfer least amount of information

Agreement with - Intermediaries + Clients

- Claims notification

- Disclosure

- How broker is paid

- How monies held

- Data protection

- Compliance

- Dispute resolution

Organisation such as LMA, IUA, LIIBA help develop template

What's inside

Really Responsible Agents Handle Compliance, Ownership, Law, Conflicts & Confidentiality.

- Hold funds on insurers behalf

- Regulatory status

- Remuneration

- Holding money & taxes

- Standard cooperate procedures

I Can Definitely Prove My Duties Clearly Defined.

6E) Broker Remuneration

- How to pay the BROKER = Flat fee client pays, must be pre agreed and intentions stated.

- Commission or Brokerage = payable by insurers.

- Other fees/commissions = Collecting commission 1% of claims, Engineering fees.

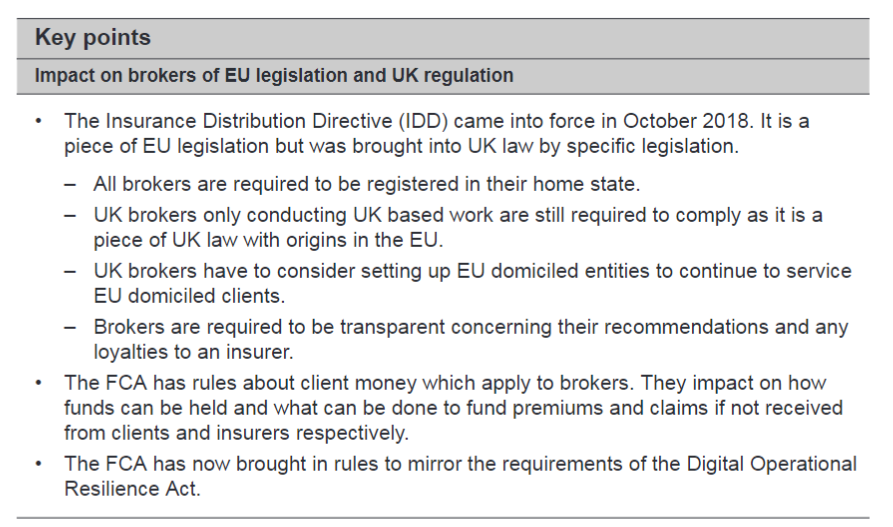

6F) Brokers impacted from EU Legislation or UK regulation

IDD - Insurance Distribution Directive

Insurance intermediaries are governed by IDD (distribution & conduct),

- EU rules for insurance distribution and conduct

- Intermediaries must be registered in their home state

- UK brokers writing EU business usually need an EU-authorised / EU-domiciled entity

- Must act honestly, fairly, and professionally

- Customer information must be clear, fair, and not misleading

- Must disclose the nature and basis of remuneration

DISCLOURE nature + basis of any remuneration

4. DORA = EU finance sector resilient to severe operational digital disruption.

FCA + DORA = test systems regularly and self assess

- EU reg which transfers to UK

- IT system testing sever operational disruption

UK CASS - (Client Money Protection)

Client Assets rules (CASS) - Protects client money by requiring segregation and proper handling by brokers.

- Statutory trust accounts - purely for clients monies. approval needed for payments

- Statutory trust accounts - pay the claim to their client before the insurer pays the money to the broker

Data protection legislation

**UK GDPR + DPA 2018 (+ DUAA) Data protection law governs

- how personal data is processed, stored, and protected.

ICO may levy fines of up to £17.5m or 4% of annual global turnover if higher.

Key Points C6