C2 - Policy Wording

SETS OUT T&Cs

How are they evidenced?

What difficulties might you face if there is a dispute some time after the agreement was supposedly made?

State make motor, employers’ liability, professional indemnity for certain professions such as solicitors, and public liability COMPULSORY

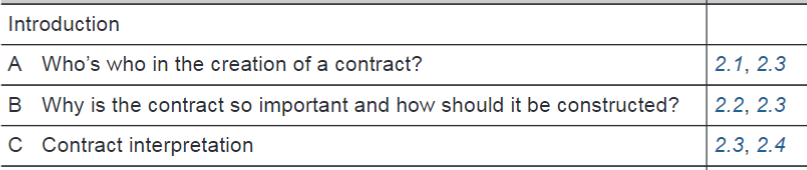

Flexibility VS Ambiguity:

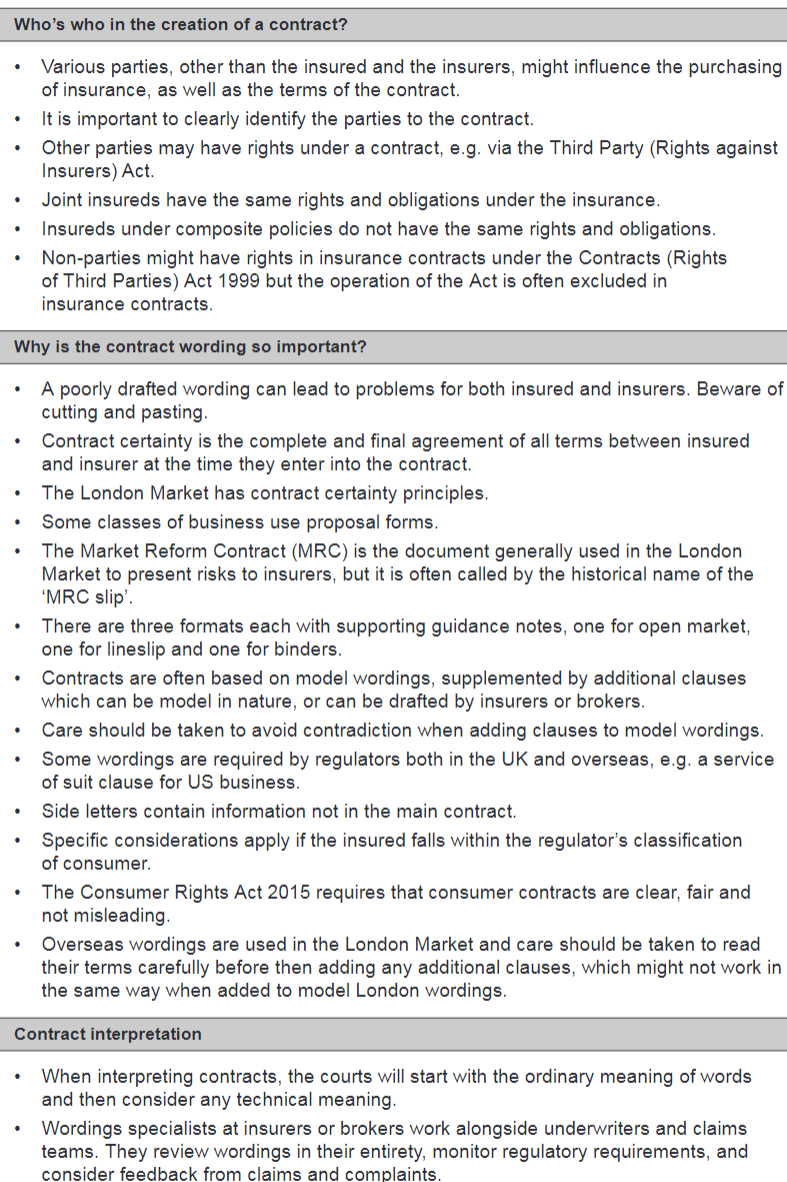

Who are the parties of the contract

main insured + additional parties

JOINT = two or more parties are insured and their interests are the same

COMPOSITE: a landlord and tenant not the same interest

A coverholder/MGA is the third party to which underwriting authority can be delegated under a binding authority

Who has right and obligation

joint policies is indivisible so if one of the insureds breach any terms WILL lead to insurers have right to invoke LEGAL remedies

IF composite then 1 entity innocent is exempt

Contract law

- Privity... who can make a claim/see insurance contract

- Third party Act 2010 - The Act lets an injured person claim directly from the insurer when the person or company responsible for the loss is insolvent

- Contract Acy 1999 -

Importance of contract and its structure

Policy limit

each and every loss?

Aggregate?

Sublimits?

Excess - Full stated policy limits SITS above it

Deductible - Deducted from stated policy limit

Cost in addition - NOT erode policy limit

Cost inclusive - (Exposure exess layer insurers or shouldered by insured) think legal cost

Policy period - include time zone and 24 hour format

Conditions - What are Renewable energy market standard clauses?

- Perils covered

- Excluded

- terms with Power of warranties

- Terms with precedent to liability

- Is Cyber crime covered?

Price - Currency value vs SOV value

LM2 - C8 - Business process#8.C) Key terms and conditions used in policy wording

LM2 - C8 - Business process#8.7 Changes to contract after agreed, approval via GUA & Endt

Contract Certainty

LM2 - C8 - Business process#8E) Contract Certainty

Steps:

- Entering into the contract

- All terms are clear + unambiguous by time offer is made

- Within TERMS... Conditions OR Subjectivities expressed

- After entering into the contract

- Final Docs shared

- Demonstrating of performance

1. - Contract changes

- Certain and documented promptly

OR

More than 1 participating insurer:

- Certain and documented promptly

- Contract contains: Agreed basis on which each insurer's final participation determined

- AVOID over placing

MRC

- Open Market

- Lineslip

- Binding authority

LM2 - C8 - Business process#8.5 Purpose + Content of OPEN MRC (Market reforms contract)

Blue print 2... MRC v3...

Value of wording libraries

broker, insurers or clients create wordings

Committees create new/update wordings (insurance act 2015 or enterpise act 2016)

Deleting exclusions will widen coverage (Look for extreme coverage examples)

Impact of broker-drafted contracts on same topic

Contracts includes other Clauses

2 separate elements of text could contradict each other.

Clients like broad Terms & Conditions + More added = increase chance of contradicition/conflict and ambiguity.

broker clauses act differently eg ROD

Regulators require specific wordings

For consumers

general requirement in the USA for a service of suit clause to be inserted into contracts

Side letters and when used

Side letters are used in matters deemed sensitive, where one party does not want information shared with wider parties which might have access to contractual documentation.

There are other uses for side letters such as:

• Clarification – side letters are often used to confirm additional details that are not known when the main documents are finalised, or to clarify certain points.

• Variation – when dealing with any last minute changes, it is often easier to set out the relevant details in a side letter than to make manuscript changes and have them initialled.

Side letters are also an efficient means of documenting any changes that have been agreed in relation to a party’s standard terms and conditions

Reverse Engineering for Wording

Used in reinsurance market -

Fronting and admitted bases

Consideration when clients are consumers

Consumer Insurance (Disclosure and Representations) Act 2012

Insurance Act 2015

Clear and unambiguous insurance policy

micro-enterprise should be treated more like consumers than commercial customers

consumer and micro-enterprise), as well as small businesses with up to 50 employees or turnovers of less than £6.5m

can use the Financial Ombudsman Service (FOS) LM2 - C10 - Claims handling#10E) Complaints Handling AND Services provided by FOS & FSCS

clear; • fair; and • not misleading.

Impact of using wording outside the london market

Lead by non-London market OR client wants wider wording

If CHANGES are made to a model wording IS uncertainty or ambiguity created

Overseas wording: check has an inbuilt dispute resolution contract e.g. a law and jurisdiction clause or an arbitration clause).

Careful using an US-based insurer wording in other countries to dispute resolution

For example LM2 - C8 - Business process#Type of Conditions precedents are + remedies for breach

are not legally recognised in some jurisdictions

c. The wording might have a different interpretation under English law.

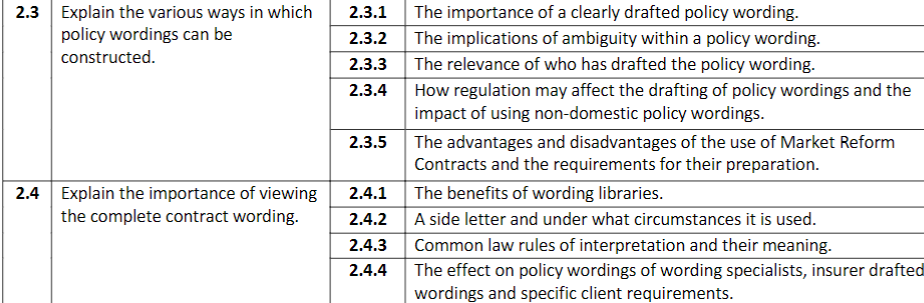

Contract Interpretation (Good as its Papers Worth)

Courts interpretation of Documents (MRC slip and Policy wording)

so if a term is deemed unfair under the provisions of the Consumer Rights Act 2015 it will be interpreted in their favour.

Common law rules of interpretation

Ordinary meaning -

technical or legal meaning -

Inconsistencies from model wording adaption were what the party intended

policy wording trumps SLIP

Interpretation issues with client contract

If the client drafted the contract (or inserted bespoke wording into it), then the client becomes the drafter — so any ambiguity in that wording would now be interpreted in the insurer's favour instead.

Role of wording specialist

Persons responsibility to check contracts fit together properly, are clear, fair, non-misleading, cohesive and above all make sense.

- considering them in their entirety for ambiguity/ contradictions

- development of new products/contracts considers Regulations and statutory requirements both home and overseas

- issues which arise from claims and complaints, and assisting underwriters and placing brokers with possible solutions

- monitoring changes in law

Wider business risk