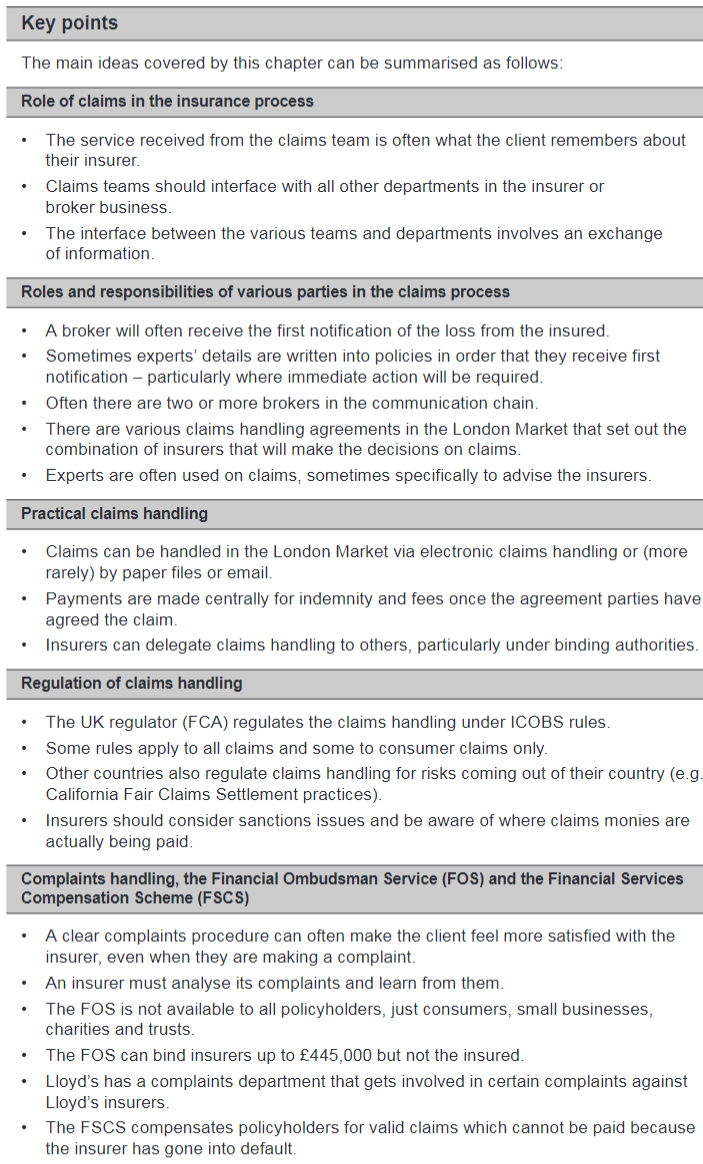

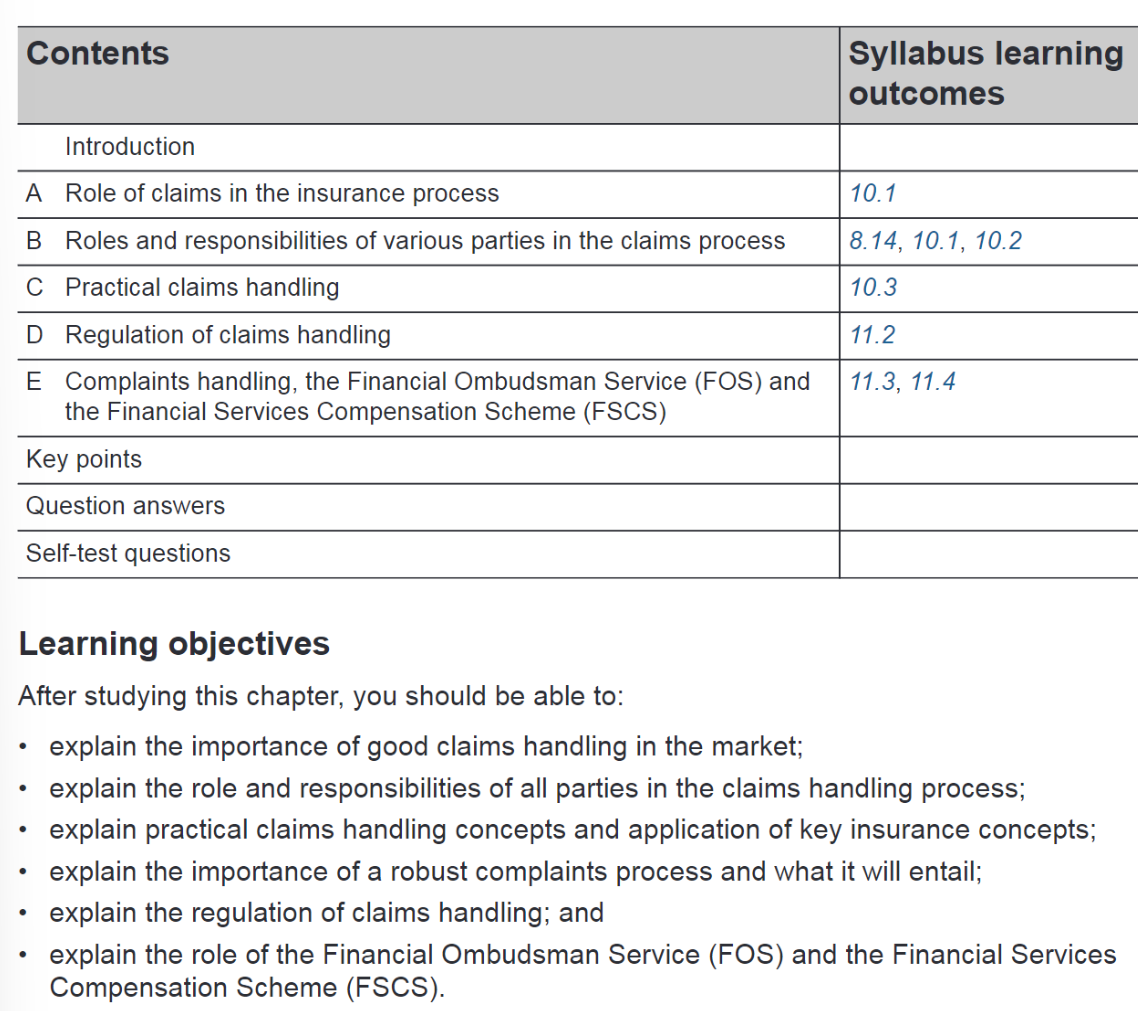

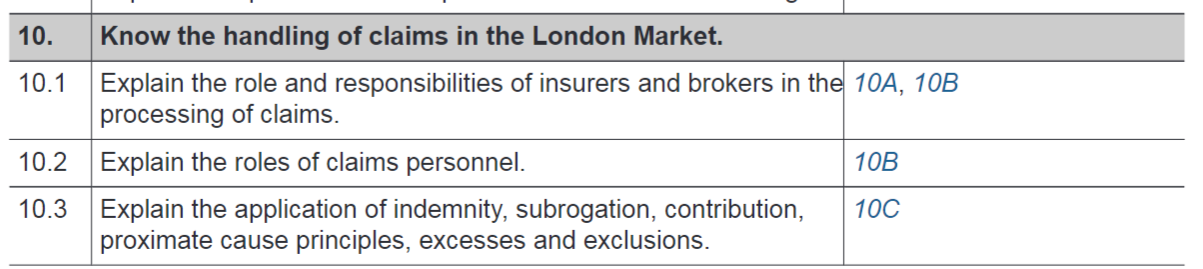

LM2 - C10 - Claims handling

10A) Role of claims in the insurance process

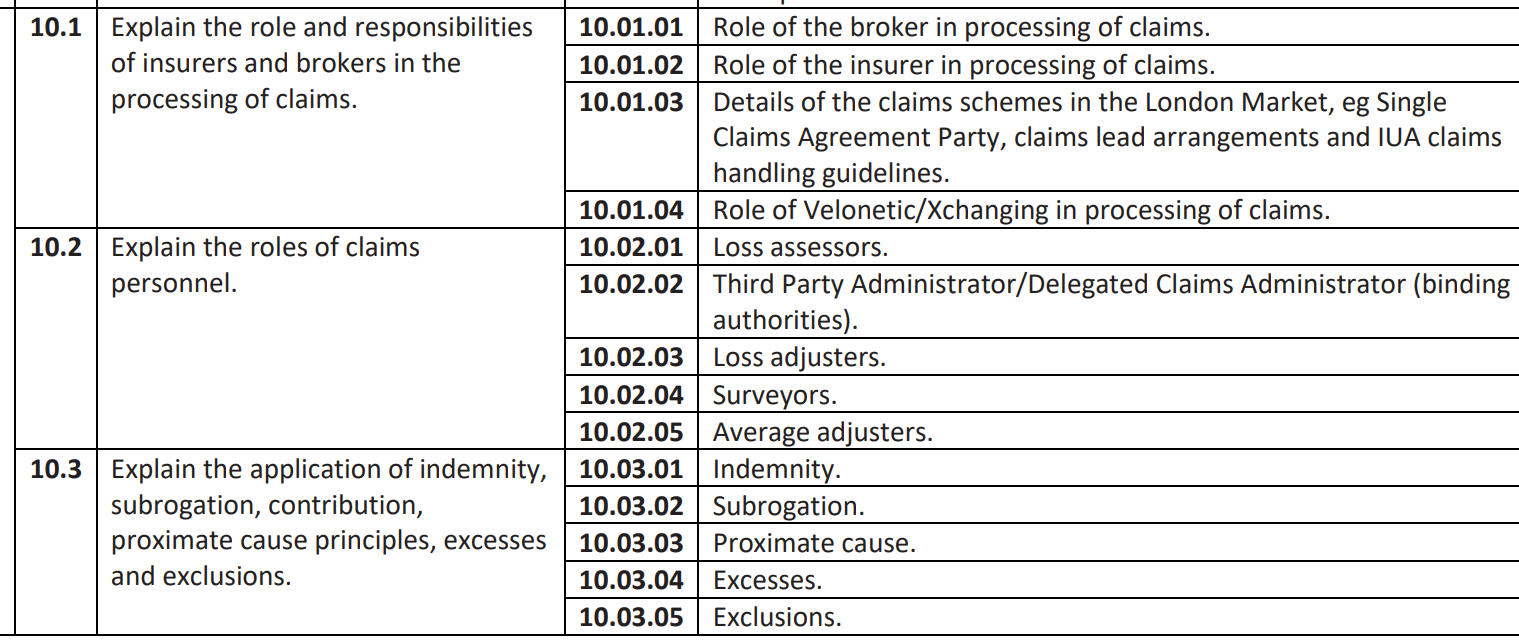

Brokers role in claims process

- First party to found out about the claims from insured = "First notification"

- If placed in London review MRC

- Negotiate on behalf of client & receive claims fund for transmission to client

Insurers role in Claims process

- Claims agreement parties mentioned in MRC

- IUA (International Underwriting Association) of London company markets

- Does London market agree to follow overseas insurers

Interface with

1. UW (wording interpretation, intent of claim)

2. Out RI (Claims control LM2 - C3 - Reinsurance)

3. Complaints,

4. MI (BI team),

5. Legal (outsourced claims, Litigation, wordings),

6. Compliance,

7. Marketing (Understanding of the cover),

8. Senior,

9. Finance (high volumes & SIZE)

Setting out the claims agreement parties:

Lloyd’s vs International Underwriting Association of London (IUA) Company Markets

1. IUA Company Market (non-marine)

Company Market are not prepared to agree to one leader binding or making claims decisions.

THEREFORE No binding possible - each insurer must agrees for its own share.

(Must set up claims agreement system)

(NON MARINE COMPANY MARKETS do not allow delegated claims authority between insurers)

2. IUA Company Market (marine & aviation)

IUA claims handling agreement:

- Broker advice or settlement

- Lloyds involvement

- Direct business (first 2 companies agree) or excess of loss reinsurance

Advice agreed by lead company market underwriter however settlements REQUIRE

- Marine business (NOT XOL)

- Aviation (NOT XOL)

- XOL reinsurance FIRST 2 companies must agree

- Facultative reinsurance (lead company only)

(code A1234 vs 3000/01)

3. Lloyd’s - Claims Lead Arrangements

A document contains basic rules -

- how many agreement parties are needed on a claim

- when one lead is enough or 2 leads required

either single or dual leader agreements in Lloyd’s. split based on

Financial test of complexity (2 LEADERS)

Amount net of deductibles/excesses

- The thresholds are:

- more than £1 million for third party business

- more than £2 million for first party business

- more than £5 million for excess of loss reinsurance

First party business: claim by the insured for loss/damage to their own property or interest

Example: factory fire, cargo damage, business interruption

Third party business: liability claim by someone else against the insured

Example: injury to a customer, pollution liability, professional negligence

Non financial test (2 LEADERS)

Claim can be classified as complex even if financials are not met even if

- usual legal

- major coverage dispute

- regulatory sensitive

- multiple jurisdiction

how difficult or sensitive is the claim?

Exceptions = term life, satellite or business written by one or 2 same syndicates

Single claims agreement party (SCAP) = LMA 9150

Streamline handling and agreement of small less complex claims

- A Binder or a Coverholder putting line down on open market subscription business SCAP applies

- Lloyd's leader agrees to allow the clause in the slip.

- < $250k with discretion given to slip leader. Applies to everyone

10B) PARTIES in the claims process

Roles and responsibility

Role of Velonetic/XCS in the claims process (Xchanging Claims Services)

Why? entering of data, sending out overnight messages

"Technical Processing" service

Leaders can delegate authority to Velonetic + Expert organisation for claims handling

Experts

Liability matters appointed via broker (Claims adjusters or 3rd opinion)

policy/MRC states named expert - cargo professional indemnity

-

Average adjusters who specialise in marine claims and will assess, calculate and present claims for particular and general average to all interested parties;

-

Loss adjusters to inspect damage and make recommendations for repairs;

-

Surveyors to evaluate loss or damage;

-

Loss assessor not instructed by insurers but by insured. only helps insurers with preparation of claims.

-

3rd party admin entirely process claims delegated by insurers

-

Lawyers defend insured or advise insurers on policy coverage (think LTL)

-

Accountants for BI type of claims

-

Subrogation specialist

Insurers set "Terms of engagement" contact/scope between insurers and experts

10C) Practical Claims handling - Application of subrogation, indemnity, proximate cause (Contribution, excesses and exclusions)

First notification of loss Insured to Broker

Broker uploads file to IMR basically and notifies insurers

- Experts can be named notification party

- Professional indemnity - insurers nominate a lawyer

- Cargo - Surveyor local goes to SITE

Conflict of Interest Handling

If claims handler for insurer conflict of interest internally or broker has delegated underwriting authority can hand over agreement party role to another insurer (check MRC) e.g.

- Two different experts sued by same problem

- Both vessels collided have same insure

- Aviation - product liability of same part (manufactures + distributors)

In BOTH systems: Agreement parties must consider conflicts:

Organisational Conflict

- Entire insurer withdraws as agreement party.

- Broker must approach next insurer.

- Insurer still pays claim share.

Individual Conflict (“Chinese/Ethical Walls”)

- Managed internally.

- File marked to ensure correct individual handles claim.

Advising the Insurers

Right combination of what insurers are liable for...

Electronic claims file (ECF): DATA + docs transfer

- Data messaging systems/database = CLASS (IMR)

- Document repository

- CREATING a UCR attaching to UMR

Electronic systems manage conflict changes more smoothly because agreement parties can be changed within the system.

Paper or electronic Electronic Claims File (ECF)

Paper: Physical file • One at a time • Manually passed • Can be lost • Location dependent

Electronic: Online file • All at once • Auto-routed • Secure • Accessible anywhere

Further claims handling

Methods used will be most suitable for all parties + claims can take 2 transactions OR years (Option for agreement parties may decide to obtain their own expert advice)

Settlements

Agreement from Lloyds market + company market before funds released!

Enterprise Act 2016 = up to 12 months to pay claims or face damages

Claims handling under binding authorities: LM2 - C9 - Delegated Underwriting

DCA = Delegated Claims Admin (TPA previously)

Delegated authorities can handle claims within authority (financial + factual limits) outside MUST go to Principle and agreement parties

Insurer provides a "lost fund" to coverholder/TPA. updated via claims bordereau. (Provide liquidity)

OR new system = Fast claims payment solution... DRAWS MONIES from MANAGING AGENT FUNDS

Velonetic/XCS - middleman of messing system THEY update brokers with regards to agreement parties outcome... pays out for negotiation happens

Practical considerations: Reviewing claims information

Claims adjusts and brokers consideration

2. Indemnity = Putting the insured back into the position before they loss. not profiting Wording have specific provisions for betterment preventing disputes on the subject at point of a claim. policy features reduce amount paid by insurer

- policy limit

- any applicable sublimit, (Internal sublimit location, peril )

- any excess or deductible applicable.

concept of underinsurance – where the subject matter insured is not insured for its full value so insurers have the right (unless the contract says otherwise) to reduce the claim by an equivalent proportion. (BI)

-

Subrogation = Insurers claim against 3rd parties which contribute to loss. Evidence is preserved by insured UNDERPINNED by policy wording. Prevent claims leakage.

-

Contribution = 2 different insurers covering same subject matter against same risk. Sophisticated methodology. Example is 100k claim 2 polices with 50k and 100k limit. pay-out will be 1/3 and 2/3.

-

Proximate cause = Think torpedo and ship sink during storm example. Or Property fire lost roof caused a rain damage. if fire not covered can't claim for water damage.

-

Proximate Concurrent Causes = If policy covers 1 but excludes the other. no claim is paid BUT if policy covers EG - A warehouse has defective insulation (gradual deterioration – not insured / or excluded). A sudden extreme frost occurs (insured peril).

-

Deductible/Excess = Excelsior Skyhawk project travels don't want to pay (Read policy wording). first paid by insurer... Insurers generally prefer the limit to be inclusive of the deductible IF NOT explicit commercial expectation is usually “on top / subject to deductible.”

-

Exclusion = Insurers question is the wording for an exclusion "STRONG"

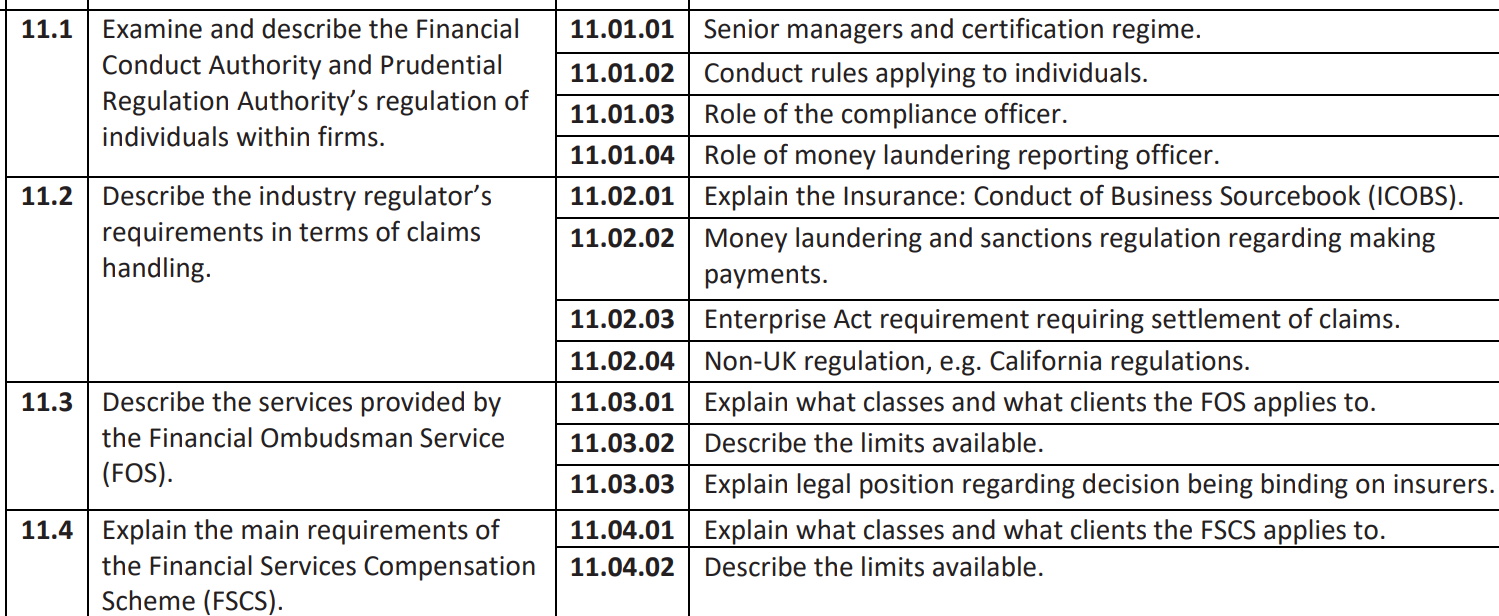

10D) Regulation of claims handling

Insurance: Conduct of Business sourcebook (ICOBS)

- Insurers are subject to stricter rules dealing with consumer insured can't apply non disclosure and misrepresentation without showing fraud has occurred!

Anti-money laundering training

Under current UK regulatory rules, regulated firms are required to ensure that adequate processes are in place to minimise the risks of the firm being used by criminals to commit financial crime (including, but not limited to money laundering).

Overseas claims handling regs = CA

claims personals need to have Certification

Sanctions CHECK Crystal+

imposed as a way of controlling the access to funds for regimes, companies or persons who are felt to be less than desirable they have links to terrorism or other unlawful behaviour.

comply with any US sanctions, as well as those coming from the UK/EU and UN.

although the insured is acceptable, the ultimate receiver of the funds is not.

Another practical problem particularly with US sanctions is that all US dollar payments will go through a US bank and therefore can be frozen if there is a problem.

10E) Complaints Handling AND Services provided by FOS

Financial ombudsman service

Dispute Resolution: Complaints (DISP) Sourcebook.

written complaints procedure...

eligible complainants. The list of eligible complainants includes:

- consumer;

- micro-enterprise with fewer than ten employees and a turnover or balance sheet total of no more than €2m*;

- charities with an annual income of less than £6.5m;

- trustees of trusts with a net asset value of less than £5m;

- small businesses with an annual turnover of less than £6.5m and fewer than 50 employees or a balance sheet total of less than £5m; or

- guarantors.

A 'directions award', telling the firm what actions it needs to take to put things right for its customer. This could include, for example, directing the business to: – pay an insurance claim that had earlier been rejected; – calculate and pay redress according to an approach or formula set by the regulator; and/or – apologise personally to the customer

Main requirements for FSCS

The Financial Services Compensation Scheme (FSCS) exists to protect insureds should their insurer not be in a position to pay valid claims

There are various limits on the compensation that the FSCS pays out, but the basic rules are: Protection is 100% for:

- compulsory insurances (e.g. third party motor and employers’ liability)

- professional indemnity insurance

- long-term insurance (e.g. pensions and life assurance)

- certain claims for injury, sickness or infirmity of the policyholder.

Protection is 90% of the claim with no upper limit for other types of policy, including general insurance advice and arranging.

The trigger for the FSCS becoming involved is the insurer going into ‘default’

unable to pay, which is usually 186 LM2/2026 London Market insurance principles

Lloyd’s can proudly state that no valid claim has ever gone unpaid in all its history.

Syndicates sometimes cease to do business and claims still need to be paid. The ‘secret’ is the Central Fund.

The existence of what is known as the Lloyd’s chain of security means that claims can be settled within the marketplace.

This means that if an individual syndicate subscribing to a risk cannot pay its share of the claim, the Central Fund will provide money once the members’ various deposits have also been used up.

Lloyd’s is a member of the FSCS.

Lloyd’s insurers (in line with other insurance companies) have to pay a levy for the funding of FSCS and this levy is also paid partially out of the Central Fund.

100% protection applies for certain categories such as compulsory insurance and long-term insurance, but otherwise the broad level is 90%.