LM2 - C5 - Regulatory & Legal Requirements

LO - C5 - Regulatory & Legal Requirements

Several regulatory & Legal aspects of insurance.

Avoidance can work against the insured

Can't lie to insurers or they will claim back (fair reps) 3rd part liability is compulsory (covers personal and national concerns)

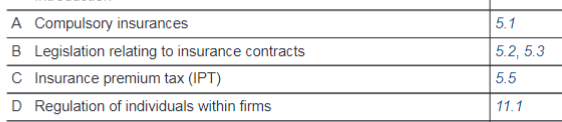

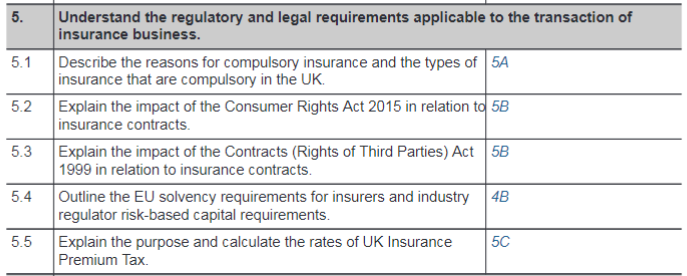

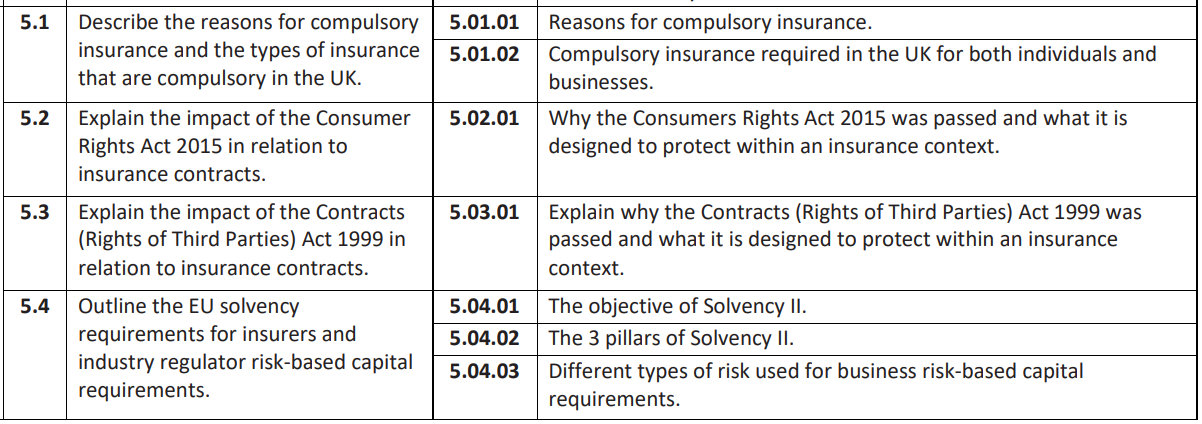

5A) Compulsory insurance and types in UK

LIABILITY INSURANCE - Financial impact of situation insure is legally responsible. Protect victims

UK composite Company Market insurers. (Aviva, Allianz, AXA) provides coverage

"Long tail business"

Why? National concerns & provide compensation

- Private individuals: 3rd party motor & public liability & animal ownership

- Professions & businesses: above + Employer's liability

Reasons for compulsory insurance

- provide funds for compensation

- In response to national concerns

Horse riding insurance + wild/dangerous animal

If a horse injuries rider or public.

Additional coverage e.g. legal fees

Warranty = promised made by insured to insurer. BUT PAUSE POLICY?

Insurers can come off risk if Breach in Duties of good faith & Fair presentation

BUT

Employers’ Liability (Compulsory Insurance) Regulations 1998

Underwriters will still have to settle claims but can take action against the insured.

3rd party liability insurer still on risk even if mispresented BUT contractual right of recovery.

5B) Legislation in Insurance Contract

5.2 Consumer Rights Act 2015

Consumer contracts ONLY = Terms & notices needs to fair

"Unfair term"

- Contrary to the requirement of good faith

- Causes a significant imbalance in the parties’ rights and obligations

- To the detriment of the consumer

5.3 Contracts Act 1999 (Rights of 3rd Parties)

‘privity of contract’. Who is allowed in the contract.

OR

It allowed certain parties, not privy to the contract, to claim on the contract.

A third party can enforce a contract if the contract expressly says they can OR Clearly identified.

Same remedies

Insurers commonly exclude the Act to prevent expansion of liability, particularly in cargo insurance, where assignment already allows claims by non-original insureds without extending third-party enforcement rights.

5C) Insurance premium tax (IPT)

UK IPT: 12% or 20% for travel

Insurer responsible for processing tax and premium. Grossed together

Insurer quotes a gross premium of £1,000 , plus £120 IPT which must be paid to HMRC.

Client pays £1000 + £120 to broker

Broker takes commission say 20%

Insurer receives £800 + £120.

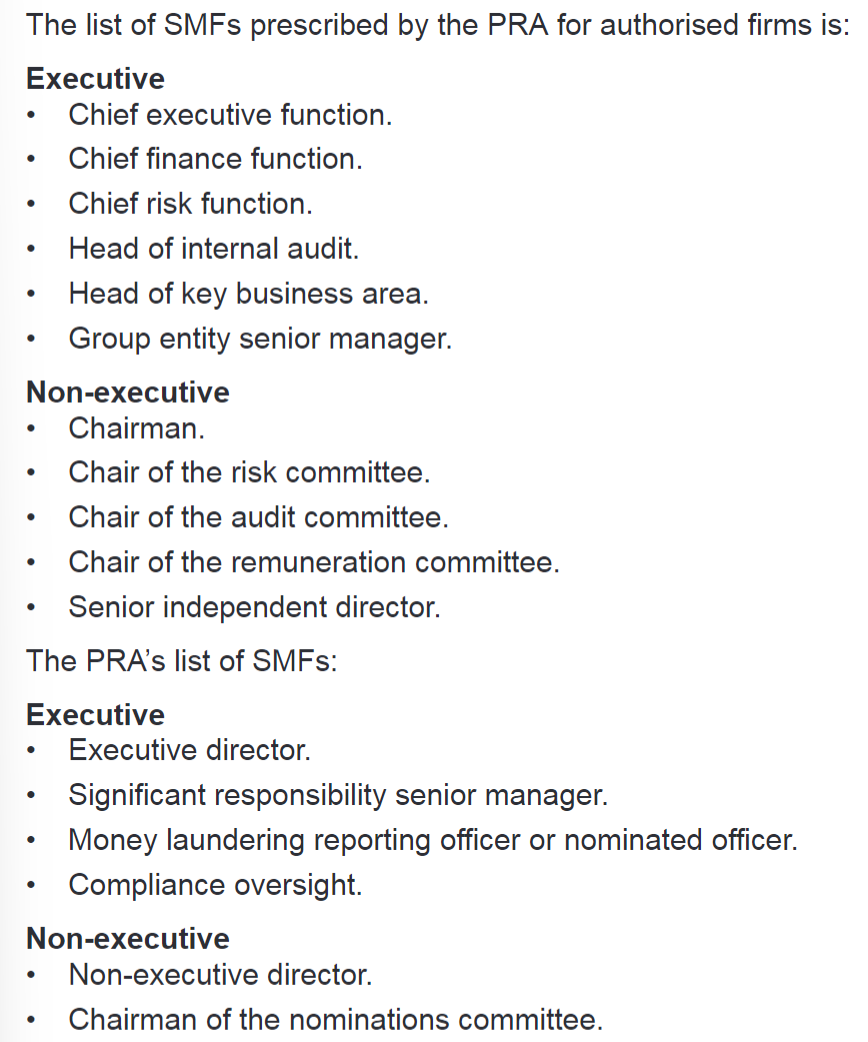

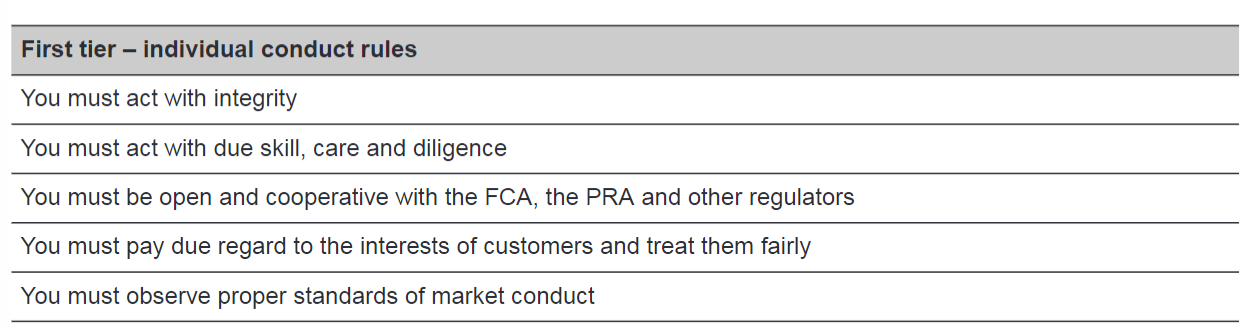

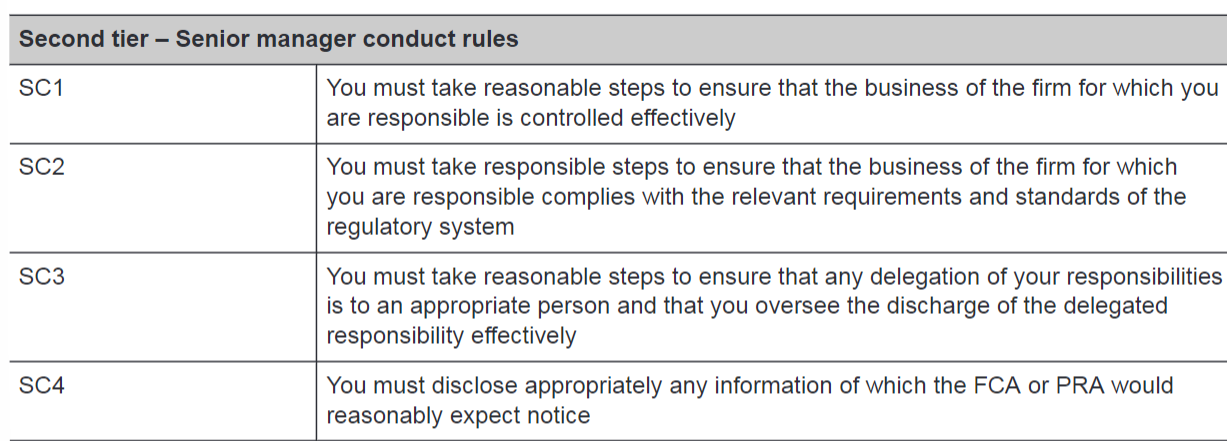

5D) Regulation of individuals within firms.

The FCA and PRA requires

Senior Managers and Certification Regime (SM&CR)

Applicable to both insurers and brokers.

Purpose:

- Encourage staff to take responsibility

- Improve conduct

Senior manager - MUST prevent regulatory breach!!!

Senior manager regime

Within organisation: Senior management functions (SMFs) follow rules made by FCA & PRA

statement of responsibilities should be prepared for each senior manager

Certification Regime

Apply to individuals who are not carrying out SMFs, but whose roles have been deemed capable of causing significant harm to the firm or its customers by the regulators.

Rules of conduct (FOUNDATION of Good Practice)

When thinking a bout tier system

1st = What can i control

2nd = what how i cede responsibility

Other behaviours to adhere

Acting with Integrity:

- Misleading

- "Approve Person" suitable of product for customer

- Preparing inaccurate or inappropriate records or returns

- Use of information