LM2 - C3 - Reinsurance

Terminology:

3.1 Why London is used as a reinsurance market

Business written in Lloyds is 31% reinsurance

- Has capacity to meet demand

- Paying claims

- Invest in new products to assist its clients

Various types of reinsurance

- How much retention of risk?

- Facultative: 1 risk being covered under the original insurance and reinsurance

- perform premium and other calculations in relation to different types of reinsurance

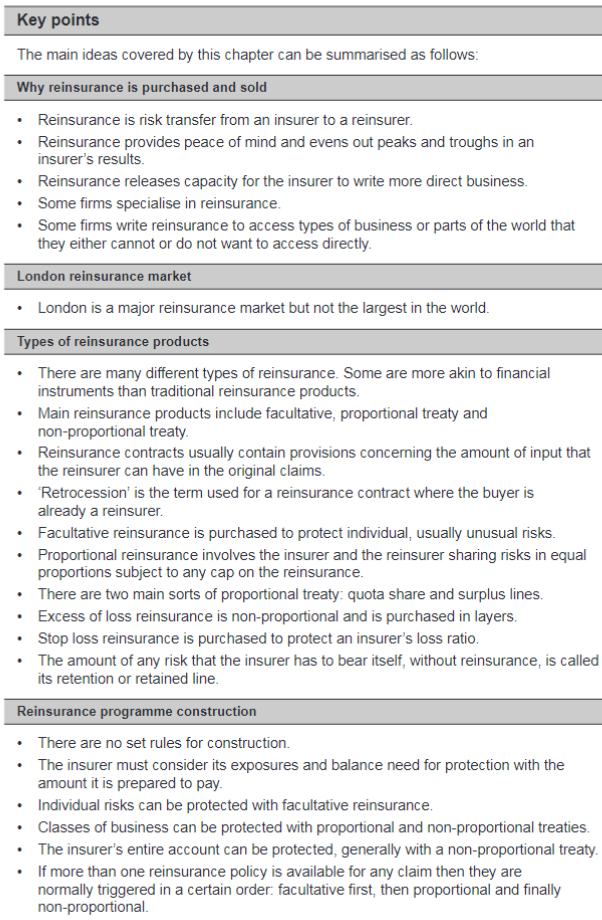

Why reinsure?

Insurers what to transfer risk they have underwritten to other insurers.

- Protection against Catastrophe-type losses financially damage business

- Some business lines are volatile, peace of mind, risk transfer

- Releasing capacity: (What is the capital invested in the business)

Writing Reinsurance

- allows access business in another part of the world without an office or operational expenses.

- Becoming involved in a COB on a trial basis, or Pure business preference

- (Regulator gives license for reinsurance only no direct business)

Reinsurance is used to increase capacity, smooth profits, reduce reserve strain, and protect against catastrophic losses.

3.2 Types of product

Full follow clause: Insurers makes all the claims = reinsurers follow. BUT must follow T&Cs in contract. Reinsurers don't like insurers extending favours with benefits. presents the reinsurer with the bill

Claims Co-operation clause: Middle ground Insurer keeps reinsurers in the loop, BUT reinsurers still lack control of process NO interfere

Claims control clause: Reinsurers have full decision making claims & failure = DELAY or impact recover of policy.

Terminology:

To cede = transfer risk with reinsurers

cedant = name of insurer who is passing

Cession = Share of the risk passed to reinsurers

Collecting note = document used to present excess of loss XOL

Fac reinsurance = 1 risk transfer

Non-proportional reinsurance = Premium and claims don't correlate (Excess of loss OR Stop loss ) = Claims paid out in excess of a pre-agreed amount.

Proportional reinsurance = e.g. 30% share of premium and claims (QS or surplus line treaty)

Reinstatement =

Reinstatement premium =

Facultative reinsurance

- Reinsurer will only respond to situations where original insurer has a claim on the risk in question.

- Insurer wants to protect a risk outside the group definition.

- Risk are placed individually = time consuming. Balance safety net vs price for fac (will it exceeds their premium income).

- Group of reinsurers or single reinsurers

Facultative Obligatory

- Cession is optional for the insurer

- Acceptance is obligatory for the reinsurer

- less common

Expected Loss Calculation

The calculation of expected loss (used to base the premium) involves multiplying the PML by the probability of occurrence of such a loss event. For example:

- PML = $60 million

- Probability (say a "1-in-50 year" event) = 2% annually

- Expected loss = 0.02 × $60 million = $1.2 million

Proportional premium and claims are shared in the same proportion as the risk ceded.

Quota-share treaty: Share 50/50 loss and premium

Surplus-share treaty: Retention line surplus is ceded to reinsurer Fractional split

- Retained line = £100,000

- Risk written = £400,000

- Ceded amount = £300,000

- So insurer keeps 25%, reinsurer takes 75%

If risk written = £150,000: - Ceded amount = £50,000

- Insurer keeps 67%, reinsurer takes 33%

Proportional reinsurance

Quota share treaty basis version equal share of risk.

add options such as

- event limits.

- Any one risk maximum limit! eg 35m

Surplus line treaty

"Lines" - Insurers has "Maximum retained line" how large can anyone 1 risk be. IF "Very good risk"

If insure does not have enough capacity eg limited to 5m (linked to Lloyds RDS, capital, Business plan)

Excess of loss reinsurance = "Non proportional"

Coverage brought and sold in layers no sharing of premium and claims by fixed percentage

- "were there any spikes in claims data",

- "Unusual/unlikely to happen again?"

- "What is the highest point?"

- Model different CAT scenarios say 5? EML

Structure

What levels do claims sit at?

Each layer can have different reinsurers

Cedant can retain 250k or 5m. "first layer vs retention"

‘working layers’ and the higher ones ‘catastrophe layers’

Pricing considerations

XOL contract will state ‘Premium US$100,000 adjustable at 5% original gross premium income (OGPI)

RISKS TO INSURERS: Cedent doesn't receive a refund!

Key terms

- Deposit premium: down payment, adjusted later (refunded)

- Minimum premium: might need later adjustment

Inefficiencies in insurance market can be exploited via reinsurance!

3. What if insurers run out of reinsurance protection half way through the year? NEED for cheap Vertical protection?

Reinstatement - bring policy back to life!

Read the QS and XOL slip.

2Question? .5x event limit. Quota share

(event limit vs aggregate limit)

And you add event limit when lots of aggs for 1 client

Claims under excess of loss

Structure if XOL spread across

- asset classes, ALL COB or

- single fac deal.

Must fall with: Any 1 event (72 hour period), claims can be grouped, CAN be abused by insurers by aggregating more claims needs to be checked by reinsurers.

collecting note = sets out details of events, financial loss.

Reinstatement premiums = non proportional + reinstatement

how much coverage total? 1mx1m with 3 reinstatements = 4m reinsurance (orginal+3)

Can structure 3 RIPs as

RIPs = Reinstatement

1. 1 @100%

2. 2 @50%

Premium same as original layer, adjusted b

Stop loss reinsurance

Similar to XOL. But linked to combined ratio CR (PI/Claims+Ops + RI cost)

Loss ratio = Claims/PI

completed e.g.

insurers buys from reinsurers trigged when CR = 105% pays out until 130% and then stop.

Think about how risk transfer are layered & priced!

Securitised risk is insurance or reinsurance risk transferred to capital market investors through securities such as catastrophe bonds.