LM2 - C6 - Insurance intermediation in London

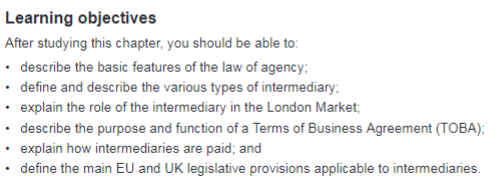

LO - Brokers in London

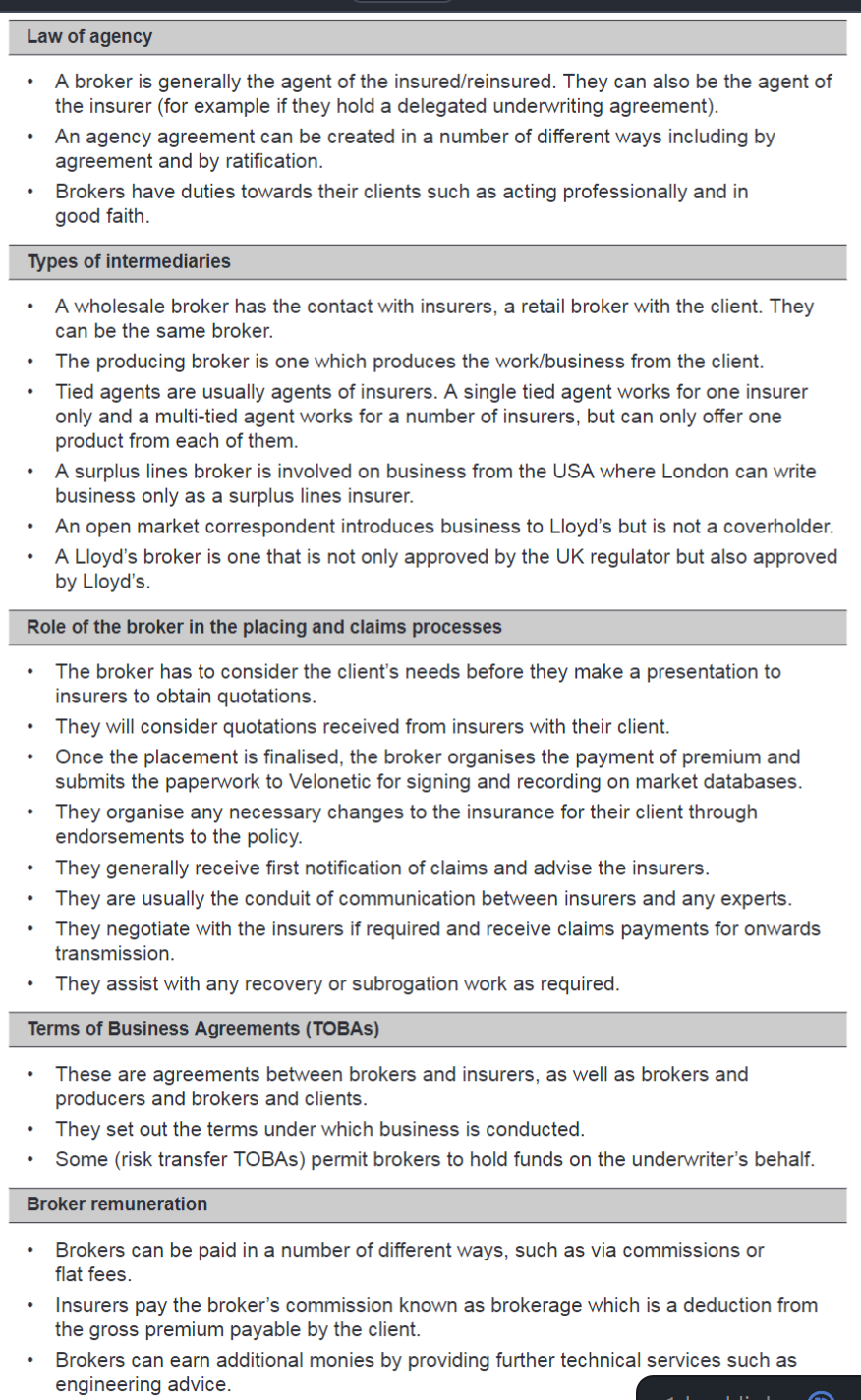

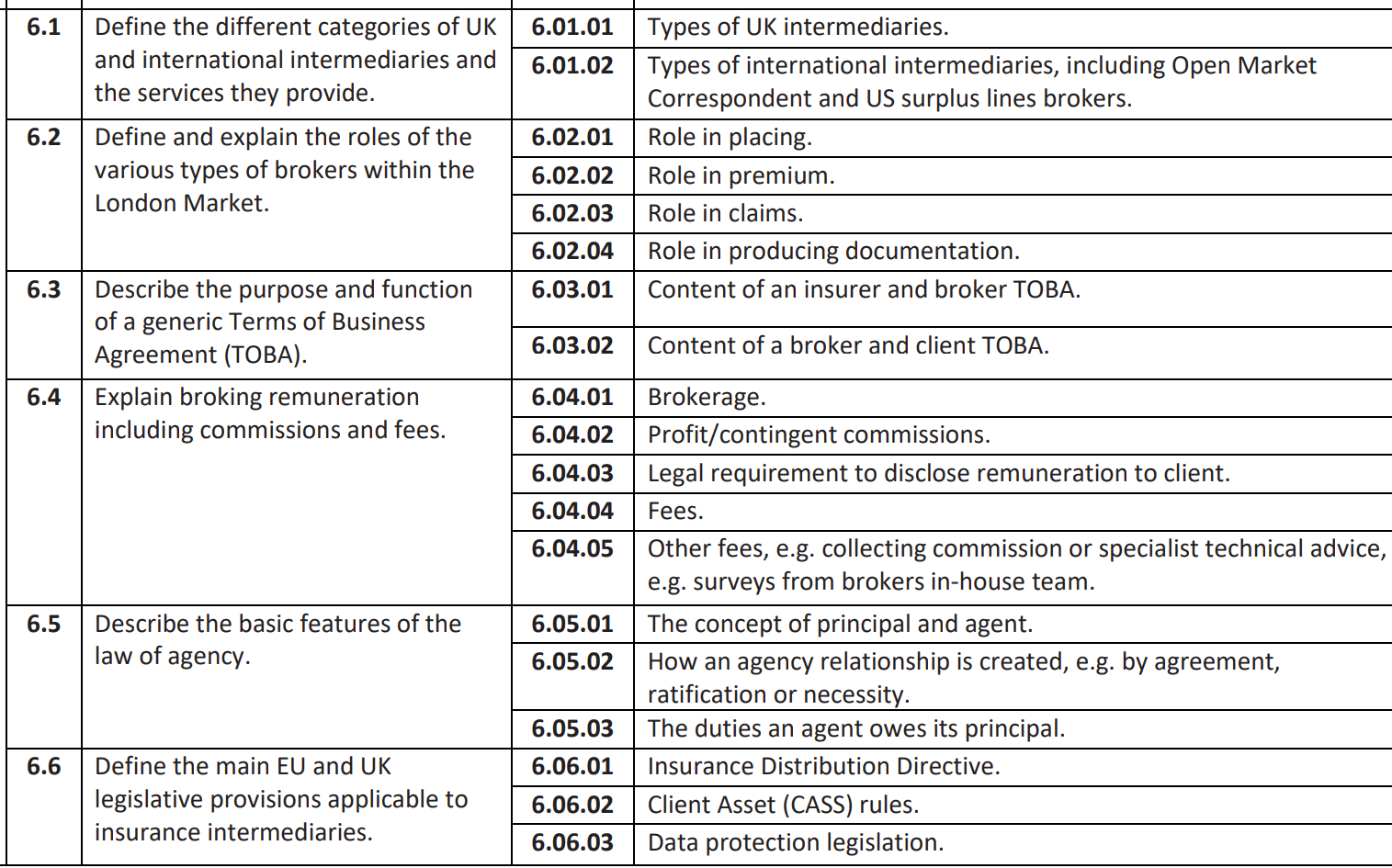

6.1 Types of intermediaries

- Wholesale - closest to insurer (People I email)

- Retail - Closes to Client

- Producing broker - supports clients with documents

- Surplus line broker - (local USA not able to take risk on)

Others

- Single tied agent - car insurer feeder

- multi tied agent - multi line insurers

- independent intermediary - FREE AGENT BROKER for client

- Open Market Correspondent (OMC) - Client => Local broker (OMC) => Lloyd’s broker => Lloyd’s syndicates (think Canada and Italy) https://www.gassltd.ca/services/energy/

Broker who PASS REGULATORY can obtain Lloyd’s accreditation.

6.2 Role of broker in placing/claims

Placing - Think about car insurance PROCESS

-

Reviewing Client's needs… is exclusion leg3 required, Securities committee

-

Putting together a SLIP/MRC to obtain quotes… survey, loss record,

-

What are the difference between quotes?

-

Finalise placement: premium payment clauses (pro rate)

-

SUBMISSION to VELONETIC: Taxes, each stakeholder is liable + Accounting & Settlement

-

Request premium from client

-

Submitting documents to velonetic allow upload to IMR give signing number & date

-

Finally: On risk and make changes via Endt.

EMAIL or PPL What types of information is included in the submission…

Influence judgement of underwriter in considering a risk

Insurers LM2 - C4 - Market Security#4D) Rating agencies

Claims:

- First advice: Presentation made considering the claim.

- Expert Instruction: Independent via insurer or assigned by broker, Fees liable to insurer

- Negotiation with claims: If hairy

- Settlement: insurer pays broker to then pass towards insured.

- Subrogation

LM2 - C10 - Claims handling#Brokers role in claims process

6.3 TOBA what's inside

A broker has TOBAs with insurers, clients and possibly also with ‘producing brokers’.

High level

AGREEMENT WITH - managing agent + intermediaries

or

Agreement with - Intermediaries + Clients

Organisation such as LMA, IUA, LIIBA help develop template

What's inside

Really Responsible Agents Handle Compliance, Ownership, Law, Conflicts & Confidentiality.

- Hold funds on insurers behalf

- Regulatory status

- Remuneration

- Holding money & taxes

- Standard cooperate procedures

I Can Definitely Prove My Duties Clearly Defined.

6.4 Broker Remuneration

- How to pay the BROKER = Flat fee client pays, must be pre agreed and intentions stated.

- Commission or Brokerage = payable by insurers.

- Other fees/commissions = Collecting commission 1% of claims, Engineering fees.

6.5 Law of agency = Beware conflict of interest

Insurer gives authority to broker but is also responsible to insured. NEED "ethics wall"

- By agreement - writing

- By Ratification - behaviour accepted/condoned

- By necessity - last resort

Duties towards principles

- No sub delegate

- Good faith

- Follow instruction

- Accounting and skilled

As they can ratify, claim for damages, 3rd party claims

When clauses are introduced think why now?

Professional negligence against brokers/intermediaries

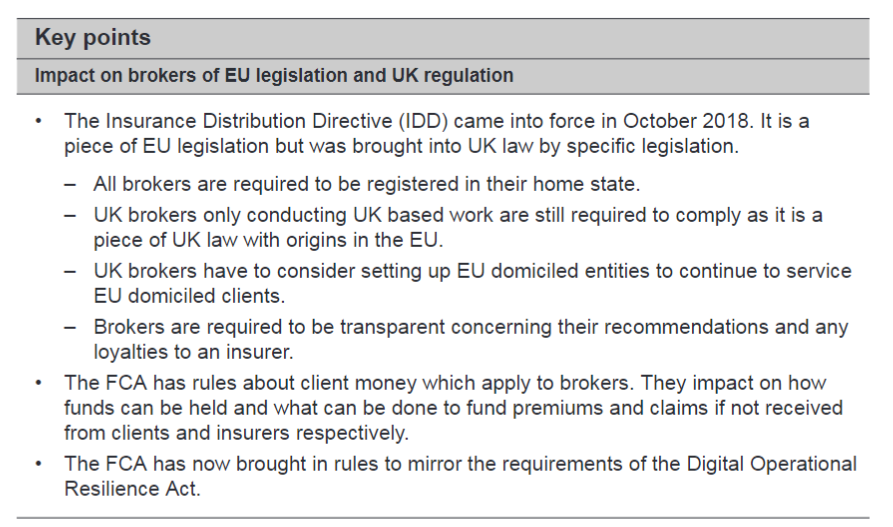

6.6 Brokers impacted vis EU Legislation or UK regulation

IDD - Insurance Distribution Directive

Insurance intermediaries are governed by IDD (distribution & conduct),

- Registered IDD in home state. a piece of UK law origins in EU.

- UK brokers need EU domiciled entities

PRINCIPLES must act fair and honestly, information should not be misleading....

DISCLOURE nature + basis of any remuneration

4. DORA = EU finance sector resilient to severe operational digital disruption.

FCA + DORA = test systems regularly and self assess

- EU reg which transfers to UK

- IT system testing sever operational disruption

UK CASS - (client money protection)

Client Assets rules (CASS) - Protects client money by requiring segregation and proper handling by brokers.

- Statutory trust accounts - purely for clients monies. approval needed for payments

- non statutory trust accounts - pay the claim to their client before the insurer pays the money to the broker

Data protection legislation

**UK GDPR + DPA 2018 (+ DUAA) Data protection law governs

- how personal data is processed, stored, and protected.

ICO may levy fines of up to £17.5m or 4% of annual global turnover if higher.