LM2 - C2 - Risk Written in London Market

lessons learnt from self test

- careful of different options wording "or" and reinstatement

- D&O coverage refine

- aviation revision loss of license focus on liabs aviation

- What are standard exclusions from each COB

- loss of earning/hire

2.1 Main incentives for choosing London market

Property insurance = 25% of Lloyd’s business, and the same proportion for the IUA companies.

- Largest in London market: split into Construction & Operational

Business areas divided into construction and operational insurances.

Why clients place business in London = They believe that they should be insured on more specialist policies.

Why some risks are pushed into specialist policies

Property insurers often prefer certain exposures to be insured under more specialist wordings/markets, e.g.

- buildings under construction (contract works)

- livestock

- consequential loss / business interruption (sometimes packaged as a separate section)

- computers (often specialist electronic equipment cover)

- road-licensed vehicles (motor policies)

- boilers/pressure plant (“own steam”)

The idea: these risks have different loss patterns and need different

- terms,

- expertise, and

- pricing.

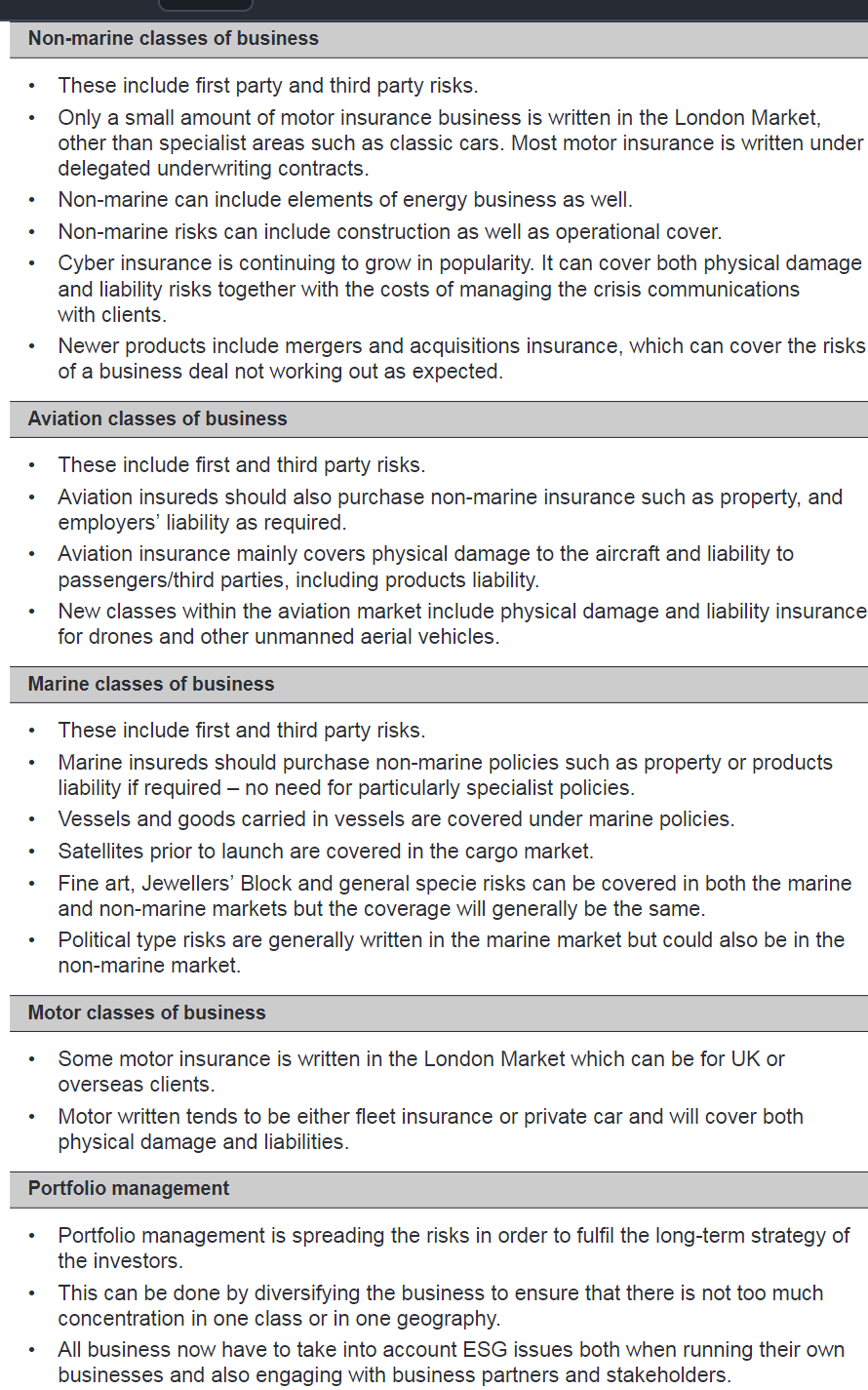

Marine, Non Marine and Aviation : Features, losses and liabilities (from claims)

Non Marine - COB

Physical Damage

- Agriculture crop, Forestry (Harvey): Weather, diseases or Hail at wrong time of the year

- Livestock: race horse becomes stallion (claims made on depreciation)

Contingency (Ravi/Rob) What if I went to a concert/event what can go wrong

- Concert or event: cancellation (artist lost voice, roof collapse, weather)

- Over redemption: more redemption than expected

- Prize indemnity: "hole in one" in a charity golf or win valuable prize

Personal Accident & Health Insurance (Toby)

- Personal accident - injury coverage + exclusion or hobbies = 'Benefits' policy payment predefined... paid out for a policy period.

- Illness/Sickness - 'Sudden onset' only + exclusion for pre-existing conditions

- Kidnap & Ransom - what makes them a target, personal security, confidentiality.

Property Insurance + Onshore Energy

Construction: Requires Specialist Contractors (Each part)

Employers

Lenders requirements/agreement AS Banks/fund source

Construction "All Risks"

==Policy period: stored prior to use till construction finish handover (optional maintenance period)==

- loss or damage to building works

- machinery movement

- business interruption

- public liability & employers liability

- damage to plant

Erection All risk (EAR) policy

Adsorbed with CAR. Purchased separately by the firms which provide

- provide Cranes or erect steelwork.

- Cover loss or damage to owned equipment

Does CAR not cover this?

How to Measurable risk as Underwriters:

- Past history? Experience of contractors in type of work

- Who/benchmark? Contractors and sub contractor

- Timeline? Contract value - updates during building process

- Where and When construction is occurring? (Season/time of year)

Operational property insurance:

- Building: Refinery chemical plant, shops.

- Machinery: industrial machines, plant fixtures office equipment.

- Stock: raw materials, production process, finished stock.

Coverage: What can Insured PURCHASE?

Fire (Underground fire), Lightning, Explosion, Earthquake, Aircraft, Riots/Strikes, malicious acts, storm, flood, escape of water, impact damage, sprinkler leakage, subsidence.

Insurers exclusion coverages negotiable: General Exclusions - overrides extensions

- Not really accidental, are Uninsurable in principle Inherent Vice (Iron rusting), failure to pay bills, war risk, radioactive, anything insured elsewhere.

- Insurers might cover, depending on the risk: Inventory shortage, pollution after perils

'Buy-backs' - theft, pay extra premium to add (Soft market difficult to push) LM2 - C8 - Business process

Exclude if not purchased

Extensions of covers: Reconstruction plans cost, breakdown/explosion. - founding in Policy wording can be subject to a sublimit

- "Expediting Expenses" - cover to pay extra costs = overtime, freight charges, parts oversea.

- ROD

- ICOW

Exclusion: Important because "All risk" policy - founding in Policy wording

- Defective engineering design: Leg 1 - 3. Applicable to all sections of policy policy structure.canvas

- What was on site before construction?

- Breakdown or explosion (Extension policy required)

- Anything Contract not liable for

- Wear % tear or Deterioration - standard property.

Reinstatement = indemnifying insured.

Insurer agrees to make good the property by taking over during period of reinstatement.

Restore to pre loss conditions or...

based on day one declared value and uplift due to inflation. Policy wording Escalation (25% + 85% submitted)

- How to check is "sum insured is adequate?"

- Reinstatement memorandum (the 85% type)... Check Policy wording

More Onshore Energy (ME)

Location – proximity to towns or cities.

- The activity – for example, is it a petrochemical plant, a power station, an oil refinery or a biofuel plant, solar farm?

- The risks being created by the nature of the activity – is the process being undertaken potentially explosive?

- What is the raw material and how is it stored?

Crime-related insurances:

- Theft insurance - Forcible entry or exit of the premises

- Exclusions for theft = Collusion, Entry gained by using tricks or keys (employee careless)

Cross over with #2.2.3 Marin COB

3. Pecuniary - Where losses is monetary in its nature rather than replacing physical or compensation from injury

Money insurance:

- Money - Insured required to transport store distribute of items being insured. Cheques stamps vouchers tickets measured by NEGOTIABILITY. how is cash handled and transferred large volumes can be insured if company is paid to do so.

- Fidelity guarantee insurance - employee stealing, checking reference, audit (sidenote coverholder)

Business Interruption

Insurers works out maximum indemnity payment during Interrupted period

Deductible = Waiting period: set up to 14 day

If property loss is declined business interruption might be impacted.

Contingent business interruption:

Indirect losses due to loss or damage at third party premises = Difficult to predict (example)

- Variation = Supply chain insurance (Insured business interruption due to another party.)

- Insured can nominate specific suppliers and supplies to cover.

Liability Classes

Directors’ and officers’ (D&O) liability insurance (Does Ian have coverage?)

- Think any decisions a CEO or VIP can make which can impact other people, includes cost of defending.

- Policies have 12 month extension but incident must happen before expiry.

- If a business collapses and loses money for its investors, a claim may be made under a D&O policy. The investors may also sue their bankers, lawyers, accountants, tax advisers and financial advisers

'Losses occurring' vs "claims made" policy

- Each and every "loss" or "claims"

Error and omissions/Professional Indemnity

Goal is to protect innocent victims

In English law, the time for making claims under most contracts is six years from the alleged breach and for tort claims

Policy wording changes for

PI insurance Accountants

Engineers

Lawyers.

Fees not paid by clients.

Claims-made (and notified), meaning the policy in force when the claim is first made and reported responds, not the year the advice was given (2017) or when the client relationship started (2014).

-

Public liability - Supermarket slips or train derails. Who to share blame with? injured person’s share of the blame is known as ‘contributory negligence’. Policies offer 10m, laws minimum = 5m

-

Product liability - Wide coverage indemnity for injury or damage occurring during the period of insurance but only against liability arising out of or in connection with any product’. EG Faulty Car! wv situation

-

Employee liability - UK is compulsory, Employers' liability tracing office. Database to track EL policies. Different rules in USA do not have NHS

-

General liability - Combination of policies above and other liability required by organisation can be abbreviated into GL

2.2.1 Non marine 'Other' insurance

Niche speciality products

-

Financial guarantee insurance: insurance can't be purchased resulting in a gain. ==event driven e.g. changes in rate of exchange, failure of companies, ==

-

Extortion/malicious tampering: physical damage to a person can lead to a claim SIMILAR to Product Recall: as it say on the tin.

-

War Insurance - Need permission to write this from Lloyds, LM2 - C7 - Underwriting Function

-

Terrorism - sperate from property book therefore govey backed reinsurance such as ATRIA & TRIA FRANCE creation of PV book think MIKI what he does.

-

Cyber - business operations depends on IT services. Coverages for lose info, digital asset protection, third party covers secuity risk breaches, legal cost...

-

M&A insurance

Aviation COB

Aviation Physical damage

Any aircraft or flighting object.

- Coverage in air,

- Ground,

- Taxiing.

Why? Branding of safe air travel.

wear and tear + breakdown or catastrophic events

brand recognitions impacts claims adjustment and implementing fixes correctly.

'betterment' ... insured receives a better part claims will reduce.

Checks and balances and where does the liability

Airline Liability Insurance

Think granular wide possibilities:

3rd parties other than passengers... property damage or personal injury caused by aircraft or persons or object falling.

Exclusions covered in other policies

- Employees

- Operational crews

- passengers

- owned property

- noise/pollution

Passenger liability

during commute and interaction with aircraft. international travel convention pay-out reagreed

geographical operating limits

illegal purposes

people experience can handle aircraft.

Airport operators liability

- premises: hanger keeper and products

Exclusions = construction work unless agreed, any thing that should be covered under a motor policy.

Hangar-keeper liability!

Product liability

Marin COB

Standard physical + Liability + Employer liability from previous section still apply

Marine Physical damage

- Vessel construction similar to buildings, who owns vessel, what is there financial structure.

- During ops = fire perils at sea, explosion, theft

- Accidents in loading, unloading, moving cargo or fuel.

- Negligence in crew causing physical damage

- Piracy or barratry.

Collision liability - ships crashing into each other

Salvage - think suez canel incident

Sue and labour - cost over runs during policy claims

Cargo - think about logistics for ordering stuff from China to UK. Hand concept which touch the process, how does the product interact with the real world.

Offshore Energy

What are the moral hazards + physical risk LM1 - C1 - Terminology in general insurance market - Legal Principles and terminology

-

Exploration - drilling, producing, shut down, plugging

- Blowout - uncontrolled release

- Control of well - In the name (when shit hits fan)

- Cost of re-drilling the well

- Pollution and Contamination

-

Construction

- Building Rig: how long, by whom, where

- Getting it on site

- Putting it together

-

Operational - once construction is completed.

-

Contractual liabilities

- covers only bodily damage arising out of the project

- Exclusion:

- D&O policy

- purchase employers liability policy

Marine Liability

Shipowners’ liability insurance

‘mutual’ the insurer and the insured are in fact the same LM2 - C1 - Business nature London Market

P & I Clubs:

Covers cargo, Collision, Crew, 3rd party liability, Pollution, Wreck removal, Fines

"seaman status" like a union supports crew legal cost.

Professional negligence insurance

Port liability insurance for public and employers liabs exposure

Other coverages in marine market

Ships loss of earnings/hire (BI insurance for ships)

Specie block = pd and liabs for trading gems precious metals valuable documents and jewellery. overlap with money theft fidelity

Fine art insurance = private and public collection museums exhibits and the stakeholder involved in transacting in art material

Cash in transit = banks moving money or ATM stock up or high deposit by customer (cash and carry)

Political risk = insured has deployed large resources to another region eg Exxon mobil in iraq

Political risk extensions = Confiscation expropriation or depreciation of assets insured = assets seized by local or regional government based evicted from country

Trade Credit Risk = loses arising from unilateral of contract from one party for no reason (MIKI). Contract frustration between governments

Bond risk = insured ask to post bond used to protect other party during contract entry.

Motor = split into private car and fleet insurance), overseas motor insurance is also written

Portfolio management and diversification of risk

What are the long term objectives of investor DURATION

Business plans defines risk appetite

Diversification = spread risk and reward across COBs + geography + customer type

Investment strategy = e.g. Lloyds members agents should consider clients risk appetite PREPARE for volatility.

ESG = Lloyds requires managing agents to have responsible investment strat using non financial risk factors in investment decisions.

clothing manufactures use factories in countries where children are working

local welfare standards

industrial pollution