LM2 - C7 - Underwriting Function

LO - Underwriting

Capacity, Appetite, Relationships, Influence , aggregation,

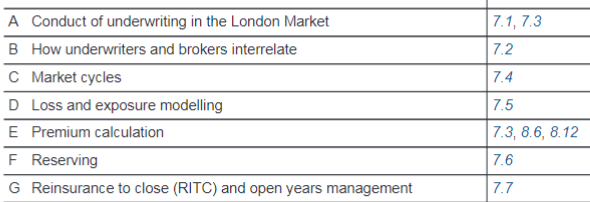

7A) Underwriting in London Market

7.1 How to Underwrite in London - "Subscription Market"

-

PINT of GLASS: Each Insurer has CAPACITY agreed by regulators + Class level

-

Appetite: Think about whole portfolio, How will a lose impact portfolio?

-

Aggregation: Potential exposure to 1 event (Fire/EQ) = TAKE smaller size know where risk is.

-

Broker influence: Risk spreading Thin or Narrow (select few vs many)

-

Insured Influence: Build relationship with insurers

Leaders and followers

ROLE OF LEADER important = represents the follow market

- International placement in London might too small + loyalty of brokers or insured request.

- Credible to other insurers that a following market will support

- Extra info LM1 - C2 - Fundamental principles of insurance

Electronic placing... research LM2 - C6 - Insurance intermediation in London

Ask a broker how is it to review lead quotations with clients? Also Thoughts on Ki insurance

Presentation of the risk

Broker presents clients risk

7B) Underwriters + Broker

7.2 Relationship between broker and underwriter

Broker as an AGENT of INSURED and Underwriters

- Agent is someone who works on your behalf – you are known as the principal.

delegate, managing agents,

Can insurer pay?

Broker assess if insurer can pay claims (LOOK AT RATING AGENCIES)

- Consider have insurer’s peers in the market were also downgraded?

Should an insurer be unable to pay a future claim then the broker may face a claim of negligence from their client.

How a broker selects appropriate market to place risk

Choice of leader

- Set good terms and conditions

- Credible to other insurers (follow market)

- Variation in deductibles and Scope Levels of coverages being granted

- Lloyds leads OR Company market lead OR mixed Bureau leads. OR overall lead overseas (MRC, a slip lead and bureau leads)

Presentation of clients risk = Full and transparent what is the information required to disclose

Duties between underwriters and brokers:

- Under the Insurance Act 2015, broker-held knowledge may be attributed to the insured for disclosure purposes, so brokers should actively help clients identify and disclose material circumstances.

- Insurer owes a duty to its investors = engaging in sensible underwriting at the right price

Insurer would have charged a higher premium, the claim may be reduced proportionately to reflect the premium that should have been charged.

FCA Consumer Duty: the 4 outcomes

- Product Governance + Target Market + Vulnerability Considerations

- Fair value assessment, distribution chain, fees, complexity.

- Clear Communication + timing + not misleading by omission

- Ease of access, quality of service, support needs.

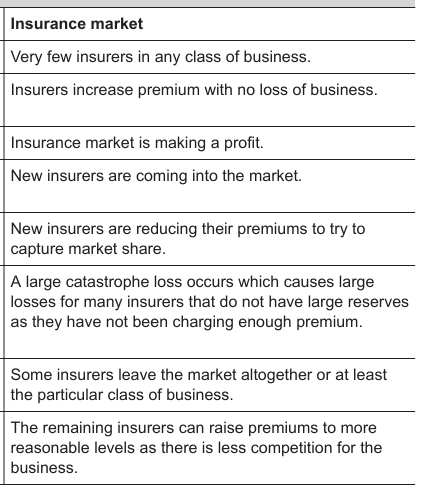

7C) Market Cycle

7.4 Market cycle - cause and effects

- ice cream seller and the fortunes of their business

- What are the dynamics at play!!!

- HAS LLOYDS AGREED BUSINESS PLAN

- Has coverage changed

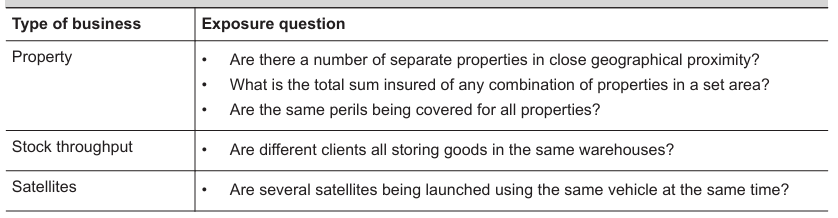

7D) Loss and exposure modelling

7.5 Exposure modelling

EML & PML

Another calculation is PML: Fire spread how will it impact loses

EML cals

How much can we keep net?

Check New Madrid

What are the 2 other lose scenarios

What was the RDS for shua

PML helps to determine how much reinsurance is required!!!

Loss modelling

RDS - Realistic disaster scenarios - Function = likely financial losses in predetermined cat event.

- Risks with exposure and maximum claim

- Net of reinsurance

- Cost reinsurance cost

- What can be covered

Gross is before reinsurance

Cat modelling

purpose of RDS Assess Frequency & severity of any event = CLAIMS VOLUME INCREASE.

7E) Premium

Premium

"Common Pool" - degree of risk insured brings to pool.

- What is Frequency

- What is Severity

Appropriate "loading" or "Crediting"

Premium base - a measure of the exposure

- Property value

- liability - payroll or work undertaken

- Product/public liability - rated on turnover

- PI insurance - fees earned ( engineering consultancy)

CHANGES with COBs in LM2 - C2 - Risk Written in London Market

Premium rate - What are the hazards? HAZARD - Which Influences the operation or effect of the peril

1. EG peril of fire with the hazard of a wood framed building

Follow market Premium

- Disclosure of follow market premium BIPAR (UK left EU)

- Broker has a lot of power to create the right insurance product for client

- Follow market can set a higher or lower rate than the lead with adjusted terms if requires to meet appetite, capacity, develop relationship with insured, aggs.

Other Premium Components

- OPEX - Doing business as insurers (Claims, office, ops, events)

- Reinsurance cost

- Profit margin (tax)

- Claims reserves build up

8.12 Premium Processing

Premium Flow: Insured → Broker → Market → Underwriter

Debit notes = A document issued by a broker to the insured requesting payment of premium + tax.

London Premium Advice Note (LPAN) = The document submitted by a broker to the central market processing system to notify the market of premium due under a contract.

Velonetic/Xchanging Ins-sure service works

Broker responsible for payment of premium under marine insurance act 1906

Changes in premium associated with ADDITIONAL documentations.

Bind → Debit Note → Client Pays → LPAN → Bureau Processing → LPSO Ref → Split by Signed Lines → Underwriters Paid

7F) Reserving provisions for outstanding liability

Assets > paid claims + unpaid claims + Ops cost

Why reserve and impacts on solvency margins

- Funds for claims in the future

- Reserving represents cost of a claim

- Cost of the claim indemnity

-0.5% personal injury claims reserving requirements

Reflects likely cost of the claims

- Cat loss

- Large loss

- Att loss

Expert/lose/claims adjuster

Consider local Regs (USA legal system or Changes in Gov Regs)

Higher reserving = greater liabilities therefore more capital

Regulators then require you to hold more regulatory capital (SCR/RBC) Chapter 4 - LM2 Solvency

under‑reserve, your booked liabilities are too low, so your balance sheet looks stronger

Short/Long tail business

Short‑tail classes (e.g. property) tend to be reported and settled quickly, so the ultimate claim cost is visible sooner and IBNR is relatively small.

Long‑tail classes (e.g. liability) have long lags between loss, reporting and settlement; over time, inflation, legal changes and new information can push the final settlement well above the original case reserve.

Incurred but not reported (IBNR)

Making provision for claims payments where the claims are not known about yet.

Incurred but not enough reported (IBNER)

Claims which are known about but for current posted reserve may not be adequate.

Trust Funds - condition of permission from some overseas regulators

Insurer are required to maintain physical funds or reserves within the particular country’s borders in relation to risks written that are located inside that country.

situs funds or trust funds = calculated using the reserves that are held on open claims within the market systems.

maintain these trust funds at the required level

7G) Reinsurance to close (RITC) open years management

Insurers group their business into years of account using UK GAAP principles.

AFTER 3 years declaring a profit or loss for the year.

If it declares a profit, the insurer releases some funds to the Names. Investors (Names) are not liable for any more claims.

A reinsurance premium has to be calculated for the transaction.

Claims still outstanding DOOR can't close

the syndicate that wants to close a particular year of account purchases reinsurance from the next year of account to cover those potential claims.

liabilities of syndicate can't be accounted

Year has to remain 'open' investor not released from liabilities

Lloyds central will step in.

commercial RITC

or run-off