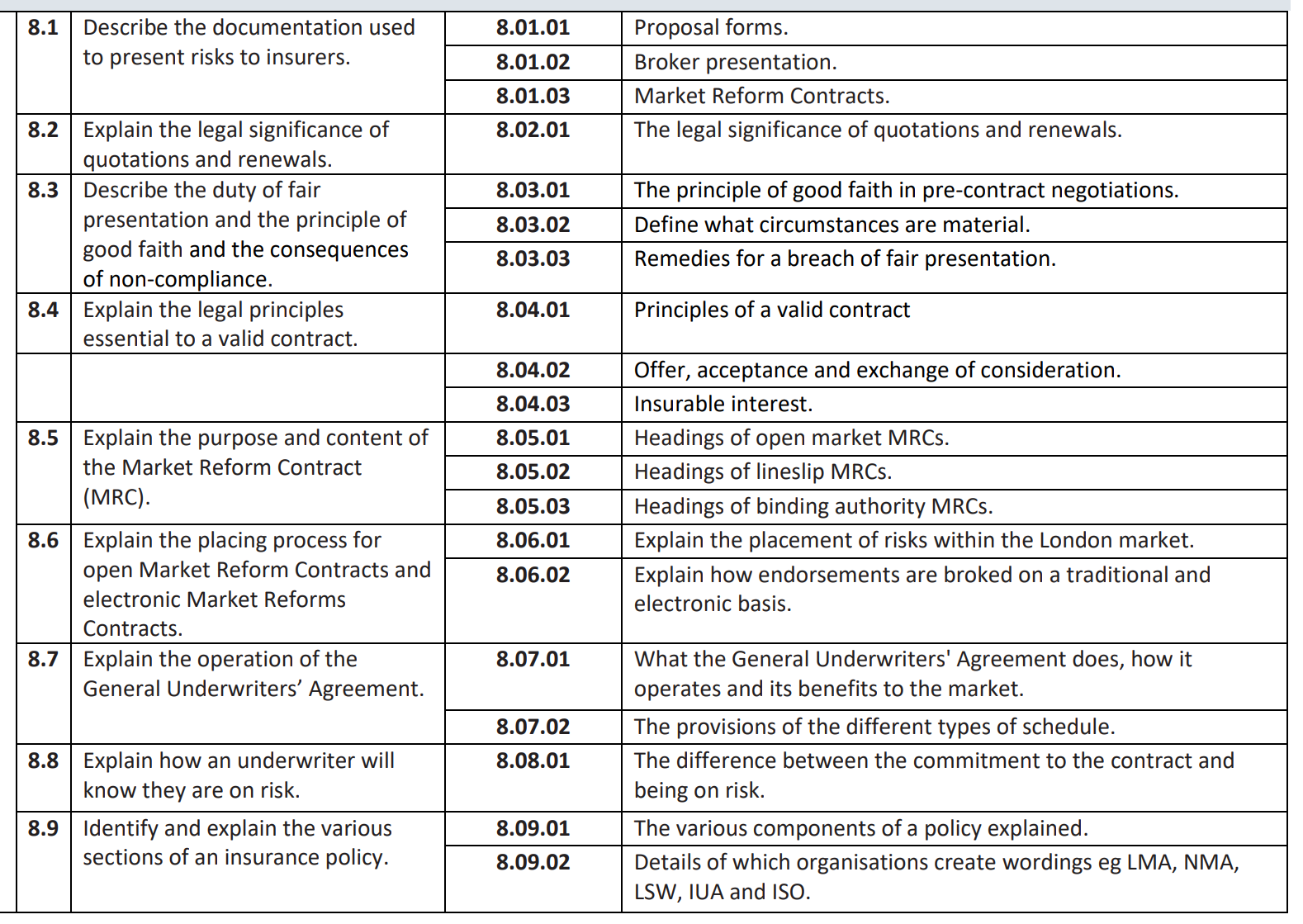

LM2 - C8 - Business process

LO

Section 8.9 has been removed over laps with 8.5 and content moved to 8.10 own section

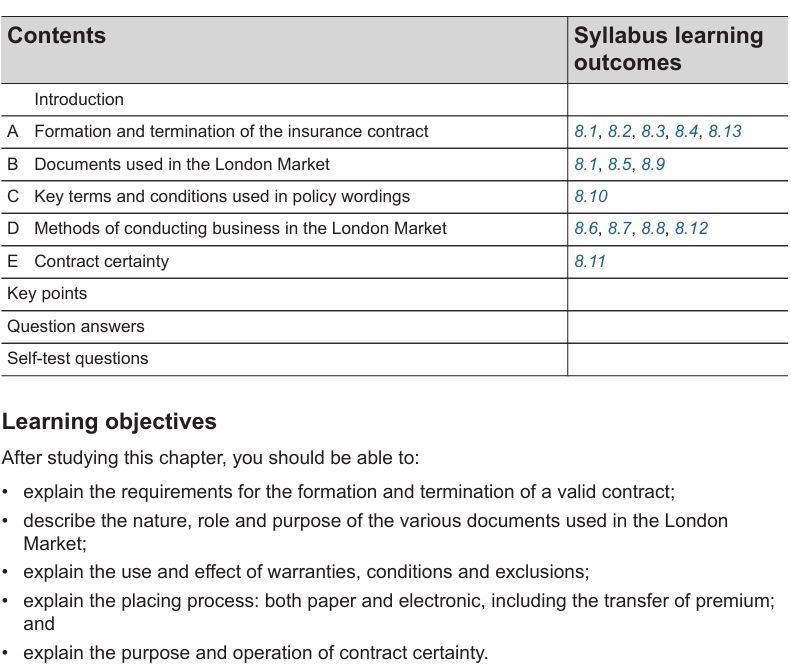

8.A) Formation & Termination of insurance contract

8.1 Documents used to present risks to insurers.

Proposal forms - Think car insurance form or YACHT/PI insurance. (Filled by assured regarding asset) by

Broker Presentation - What are Client/broker telling us?

- Is it all "Material Risk" or basis for more questions.

- Surveys - Construction phase, geology report, hydrology report,

- Data - revenues, technical specifications, FATs + SATs documents are they done by 3rd party? Commissioning document (BUILD QUAILITY)

AS A RESPONSE Market Reform Contracts (SLIP) created in the form of:

Open market business - Broker to individual underwriter 1to1.

Line slips - lead underwriter approves binding of follow market.

Binders - Underwriters give delegated underwriting authority

Insurers have 1 shot make it count...

If insurers accept the form without following up on any missing information, it will be very difficult for them to argue non-disclosure on the basis of that information at a later date in the process.

8.2 Legal Significance of Quotation & Renewals:

Step 1: Proposal/Quotation

Broker request underwriters to consider their client.

"What lead terms can be offered?"

Insurer propose T&Cs + Premium for given risk. Have to balance coverage & Premium cost.

REMEMBER! Broker + Client must disclosure material facts.

Step 2: After Quotation. Client selects preferred option.

- Stamp

- Scratches the slip with date

- Share of the risk

Step 3: Renewal

Market courtesy for brokers to request for renewal quote.

Market has changed over 12 months. MORE CAPACITY Insurers will need to Quote again STEP 1. Consider:

- Has CONTRACT been Loss-making?

- Is Insurer exiting class of business?

Savings - Time element: Less cost to renew business (Underwriting already done)

- Stable the portfolio of clients = reliable statistical data

Brokers need to ensure "No gaps in cover for clients"

Insurers check for Risk renewed late?

Stated in slip

"LINES OF WHOLE" vs "LINES OF ORDER"

&

Oversubscribed - adjust "Written line" to "Signed Line"

If good risk = Underwriter can chose "LINE TO STAND" option

On risk - Once stamped, or electronically

Fitting boxes!

Broker's can't increase written line without permission.

Writing a risk after inception

- ASK FOR LOSSES INBETWEEN PERIOD... ADD WNKORL to email

Legal Implications

- HAS to be TIME BOUND e.g. hold cover for "2 weeks"

- Client agrees past date NEED Permission

- If client accepts. INSURER CANNOT BACK OUT

- However, if terms are changed the offer lapses.

- Emails can bound risk.

8.3 LM1 Duty of Fair presentation + Good Faith + Consequence of non-compliance

the insured does not have to disclose a material circumstance that lessens or diminishes the risk. The Insurance Act 2015 preserves this exception

Duty of Fair presentation

Before entering into an insurance contract, the insured must make a fair presentation of the risk to the insurer.

- Disclose every material circumstance they know or ought to know, OR

- Give enough information to put a prudent insurer on notice that it needs to ask further questions

- Present information in a clear and accessible manner

- Ensure representations of fact are substantially correct

- Ensure representations of belief are made in good faith

- Deciding whether to take the risk, or

- Deciding on what terms (premium, exclusions, conditions)

Remedies for Breach of Fair Presentation - depend on the insurer’s state of mind and what they would have done if properly informed.

8.4 LM1 Legal principles essential to a valid contract.

Offer and Acceptance

Contract comes into existence when one party makes an offer which the other accepts unconditionally.

- Acceptance must be a mirror image of the offer.

- If any term is altered, no contract is formed; this constitutes a counter-offer.

- In insurance, a quotation may constitute an offer.

Exchange of Consideration

The promise to provide cover (i.e. to be on risk)

Insurable Interest

Required to create a valid insurance contract...

ownership or exposure to liabilities to others under the law of negligence.

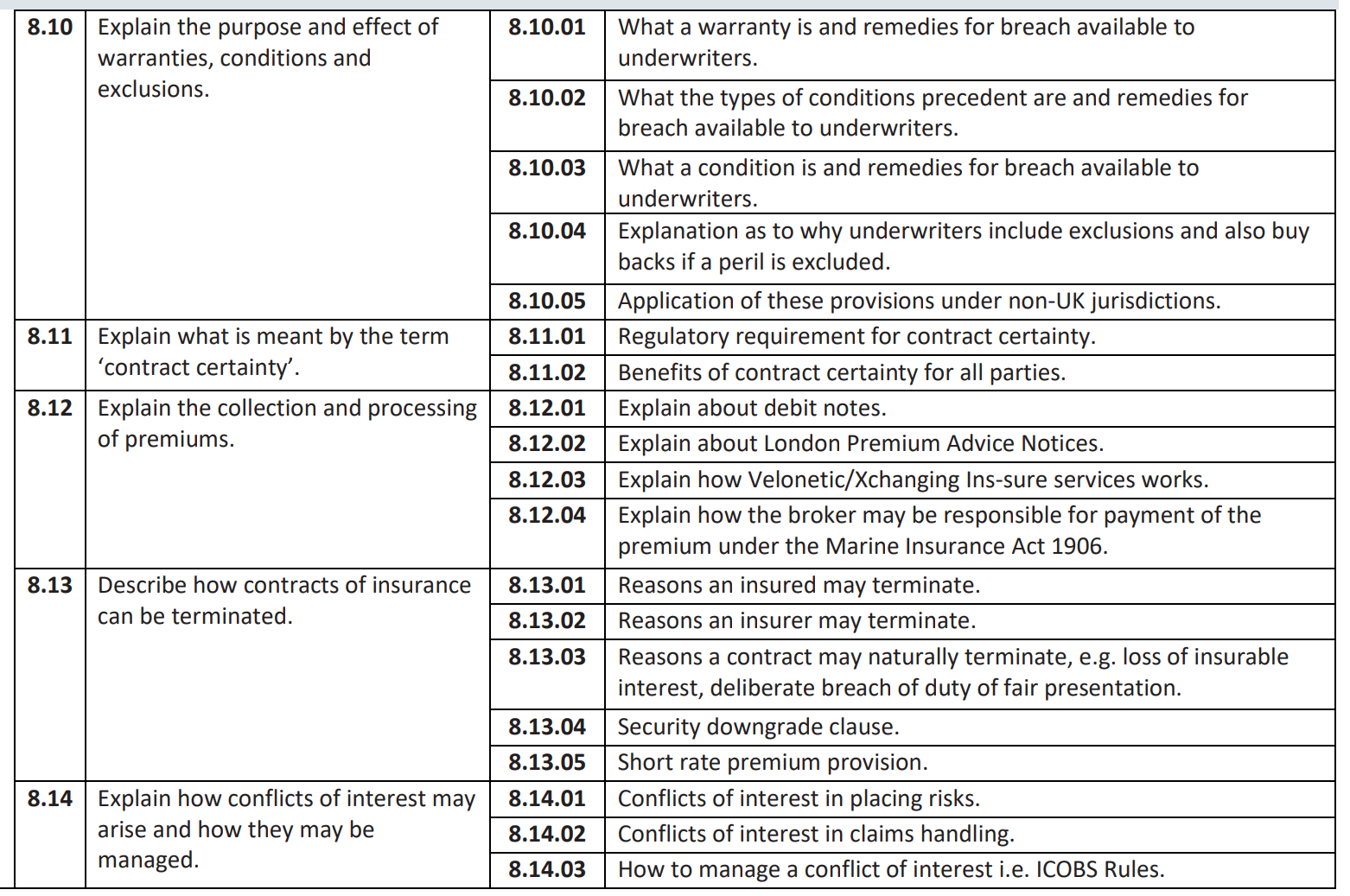

8.13 Termination of insurance contract

CANCELLATION by either parties

- By Insured = commercial reason, policy wording + Downgrade of insurer

- By Insurer = Material change... Should Marine hull be sold or SERVED PURPOSE

- Fulfilment = Single Vehicle damage, policy pays out contractually obligated (loss of insurable interest)

- Period expiry

Unexpected Termination

BREACH of duty of fair presentation:

- Breach of Warranty: Off Risk for certain period

- Fraud: Legitimate claim EXAGGERATED. or Fraud in relation to a breach of the duty of fair presentation. Insurers can keep premium

- If premium is under paid or risk change due to material info not disclosed. CLAIMS are reduced by same percentage.

8.B) Documents used in London market

8.5 Purpose + Content of OPEN MRC (Market reforms contract)

Basic PUROSE risk info

- Summarise client's risk

- UW indicate their written line

- Document sent to client

3 types - Open market, Line slip, Binding authority (Binding authority MRC LM2 - C9 - Delegated Underwriting)

SLIP - Risk Detail

Standard policy stuff at tops of slip: if soft market.

UMR, Type (CAR, PD, BI, liabs), Insured name & Address, PERIOD, Insured Interest, Limits of liability, additional limits, Sublimes, Insured Retention, Policy wording.

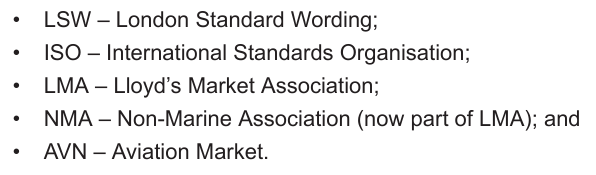

Terms & Conditions which insurance is layered on LMA or LSW or NONSTANDARD WORDING, definitions e.g. Substation, Wind Turbine Generators

Subjectivities = PROVISIONS or Time constraint placed on insured to provide additional "Material information" Before policy is active.

- Notice of cancellation provisions

Premium (Payment Term) - LSW3000 Clause = Premium not paid insurer can give 15 day notice before cancelling policy.

Don't forget Taxes, Loss Payee (who is pay claims).

For Brokers - Broker Insurance Document (BID)

SLIP - Information

Insurers liability or SOV coverage

What was shown to insurers

SLIP - Security details

Order placing on this MRC = 1-100%

ORDER SIZE: X% of 100%? or WHOLE 100/100

1. Percentage of Whole = 10% line of whole

2. Percentage of Order = express written lines against the broker's order can get signed down

3. Part of Whole - financial terms

Signed down provision: line to to stand,

Written line.

SLIP - Subscription agreement

- State who is Slip & Bureau Leader

- Basis of agreement to contract changes: GUA - #8.7 Ops of GUA. How? Why?

- Claims agreement LM2 - C10 - Claims handling

- Claims Administration, Expert Fees, SDD

- Notice of cancellation

- Bureaux arrangements: De-linking = risk sent to velonetic ASAP for database entry.

Important players: Velonetic & Xchanging

Who is the underwriting claims lead?

SLIP - Fiscal & Regulatory section

- (local and international pay attention to Lloyds market)

- Tracking Tax payable, country of origin, overseas broker, Lloyd's Brussels.

- Surplus line broker - If direct business state who the surplus line broker (!).

- PREMIUM CODE allocation = R2, R4, T6

- Commercial Large Risk (class)

SLIP - Broker Remuneration & Deductions

- Retail and Wholesale broker or other brokers,

- Brokerage amount.

- Fees

- relationships with underwriters

Digitisation: MRC v3 & Core Data Record.

- Premium validation and settlement (Lloyd's and companies).

- Claims matching at first notification of loss ( Lloyd's and companies).

- Tax validation and reporting (Lloyd's only).

- Regulatory validation and reporting (Lloyd's only).

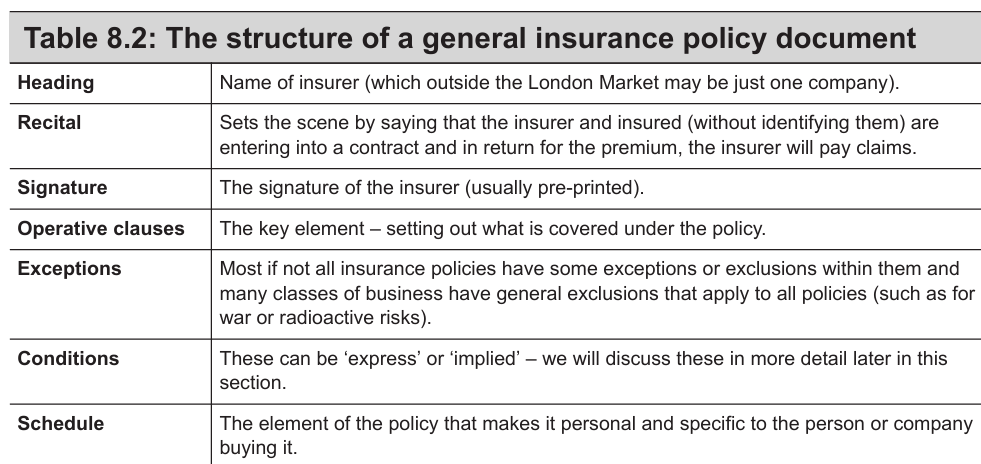

8.C) Key terms and conditions used in policy wording

8.10 Policy Warranties, conditions and Exclusion

Key terms and conditions used in policy wordings policy structure.canvas

What type of Conditions precedents are + remedies for breach:

For the insurer to have any liability under the contract.

-

Condition Precedent (CP) to Contract = Something that must happen before the policy comes into force. No condition met = no contract

"Cover for the solar farm is subject to a satisfactory X survey."

-

Condition Precedent (CP) to liability = Something the insured must do before the insurer has to pay a claim. Policy exists, but no compliance = no claim payment

"Immediate notification of cable damage is a condition precedent to liability."

Results in a total loss of coverage for that specific claim

Condition precedent:

“Notice of loss must be given within 30 days as a condition precedent to liability.”

General conditions What is the intention and effect of wording!

Exclusion - why & also buy backs if a peril is excluded

- Risk that the insurer will not cover under a particular policy

- What types of exclusions come up most frequently?

- Option to add Buy-back or write-back

see LM2 - C2 - Risk Written in London Market#Coverage What can Insured PURCHASE?

What is Warranties & breaches?

A promise made by the insured relating to facts or performance concerning the risk. or promise that something is true or will be done.

Insured reduces ambiguity by stating something will or will not be done or facts exists or does not exist.

EXMAPLE of warranty

"warranted that all wind turbine maintenance will be carried out every 6 months." or "WNKORL"

POWER TO COSUMERS - Under the Insurance Act 2015, if there is a breach of warranty the policy is suspended until the breach is remedied and the suspension lifts automatically.

What types of warranties come up most frequently.

"Insurer is considering the particular perils and hazards of any risk, they might want to put controls around matters such as the use of security devices, the safe use of machinery or how many people are on site at any point in time. These are exactly the types of conditions affected by the Act."

==The Insured "Burden of Proof" think sprinkler off during building fire ==

Risk details or policy wording will have Sources of wordings and clauses

insurers operating in the London Market choose to use another market’s policy wordings, as that other market has in fact led the risk, or is writing the primary layer when London is providing the excess layer coverage

- English law and practice.

- Insurable interest clause.

- Sue and labour clause.

- War and nuclear exclusions.

8.D) Conducting business in London Market

8.6 Placing process of open MRC & eMRC (7E, 8D)

Models for placing in the London Market

1. Service company

Alternative to sourcing deals - delegated underwriting

Backed by managing agent/syndicates

2. Branch offices:

Write business in local market with Branch. Or via Lloyds regulatory permission centrally

3. Services (cross boarder) and establishment (local office) business

Lloyds Brussels:

- Each risk written is wholly reinsured back into the Lloyds syndicates.

- Underwriter stamp looks different.

4. Delegates Underwriting

Delegation means asking and authoring on you behalf to obtain business - LM2 - C9 - Delegated Underwriting

How Endt are broked on a traditional & e bases... LM2 - C7 - Underwriting Function

Presentation of the risk

Broker presents clients risk

- Insurer delegates any authority for underwriting/settling claims

- Underwriters have a duty to produce a return on their investment. What is the "right Price"

- Insurers should provide positive outcomes to insured

8.7 Ops of GUA. How? Why? related to Endt

Endorsements are broked

Changes to the slip/contract. Establish process for AGREEING changes.

Document to present changes to underwriter & client informed.

GUA Provisions different schedule

An agreement between insurers subscribing to a risk that certain endorsements need to only be agreed by a subset of those insurers.

Purpose:

- Agreement between all underwriters on a given MRC will deal with contract changes. (Mini contract of delegation)

- Clarify AUTHORITY of leader and identified underwriters to agree changes

- Tailor to each COB

- Ensure all underwriters are notified of changes even not involved

These schedules are divided into three parts, each indicating what type of changes can be agreed by a certain combination of the insurers on the risk, as follows:

Part 1 – slip leader only (note this is not bureau leaders).

- Anything that the slip says can be changed by leader only

- Typo

- Any changes reducing monetary exposure (eg turbine decommissioned)

- Restriction in coverage (coverholder is restricted from extending cover beyond the scope agreed in the delegated authority)

- Return premium if provided for in the slip (TSI decrease or LC)

- wording amendments require agreement of the slip leader only

Part 2 – slip leader plus agreement parties.

- Anything provided for in MRC to be agreed by leader and agreement parties

- increase in deductible to reduce premium

- Wording amendment if stated as leader and agreement parties.

- claims notification period

- Anything that does not fall into Part 1 or 3

- Insured changes O&M contractor

- Risk survey frequency (SSE dogger bank Monthly updates)

Part 3 – all underwriters.

- Anything that MRC says has to be agreed by all underwriters. (Agg limit)

- Anything that slip leader or agreement parties feel should be agreed by all underwriters. (BESS addition to solar farm)

- Changes to geographical scope. (UK policy need for Ireland assets)

- Policy Extensions in Excess of 30 Days (3 month extension)

- Changes to Jurisdiction of the Contract (English law to German law)

- Backdating of the Policy Period

Remember

Overall leader: broker states terms that the leader has set.

Slip leader: London market lead

Bureau leader: First Lloyds leader

LM2 - C9 - Delegated Underwriting#9A) Purpose and types of delegated underwriting

8.8 How underwriters know if "ON RISK"

Commitment to the contract (Support broker)

- The underwriter has agreed to participate.

- The slip has been scratched (or electronically agreed).

- The written line is recorded.

- The underwriter is legally bound to the contract.

On risk (Liable transferred)

- The contract has incepted.

- The policy period has started.

- Any subjectivities required for attachment have been satisfied.

- Cover is legally active.

8.12 LM2 - C7 - Underwriting Function#7E) Premium

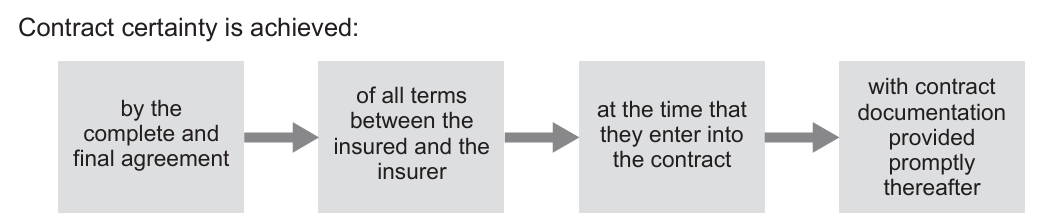

8.E) Contract Certainty

Regulatory reequipments

What is?

Complete and final agreement of all terms at the time the contract is entered into, with documentation provided promptly.

Steps:

- What must be done at inception

- After inception

- During changes

- In subscription markets

- If errors occur

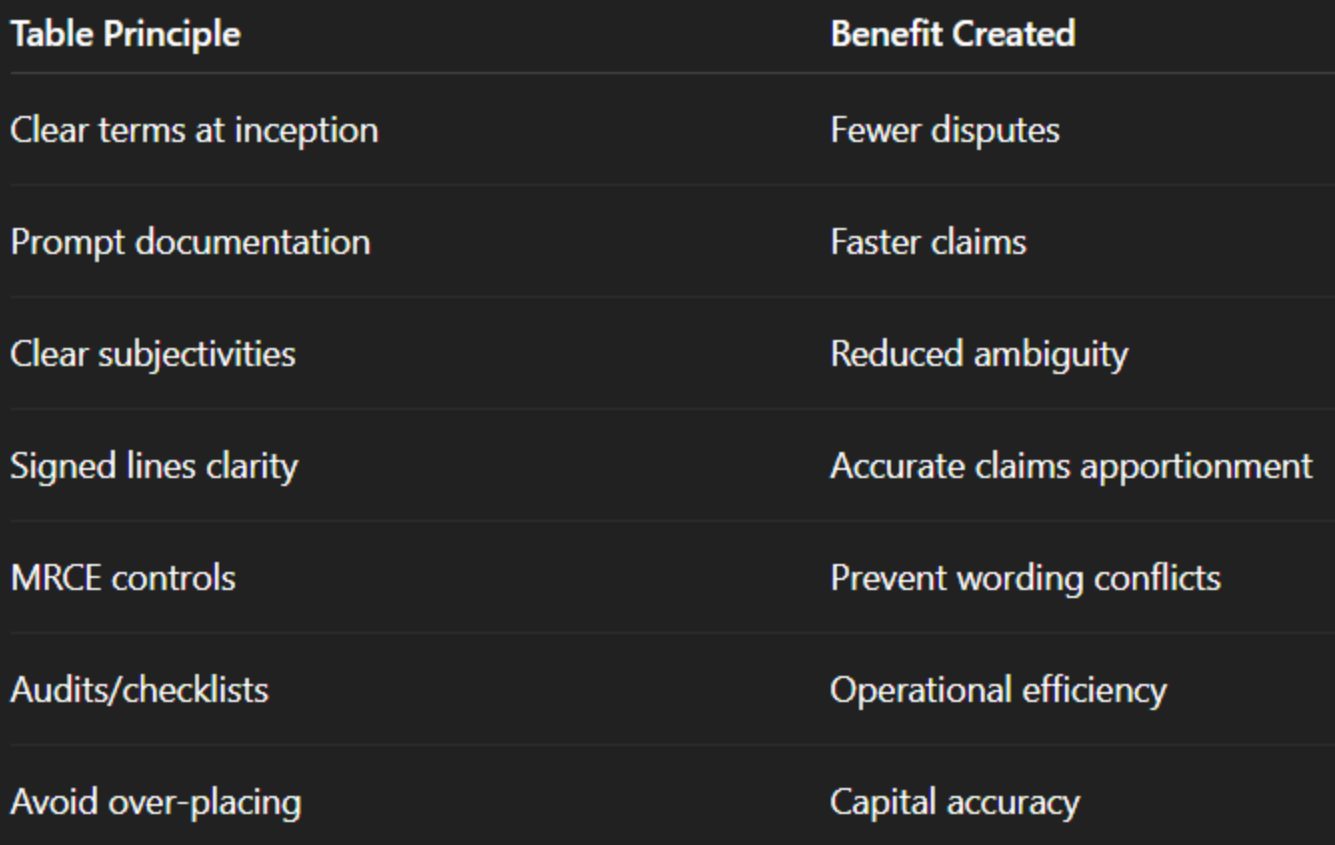

Benefits of contract certainty for all parties

Benefits of Contract Certainty for All Parties

The contract may already exist when terms are agreed, even if the final policy document is issued later

8 Key points